Margin of safety formula: calculate your sales buffer

Learn the margin of safety formula so you set a buffer, protect profit, and plan growth with confidence.

Written by Shaun Quarton—Accounting & Finance Content Writer and Growth Marketer. Read Shaun's full bio

Published Friday 13 February 2026

Table of contents

Key takeaways

- Calculate your margin of safety using the formula (Current sales − Break-even sales) ÷ Current sales to determine what percentage your sales can drop before reaching break-even point.

- Aim for a margin of safety between 20% and 30% as a healthy buffer, though businesses with high fixed costs may need larger margins to absorb unexpected market shifts or cost increases.

- Use your margin of safety to guide key business decisions including setting sales targets, adjusting prices, controlling costs, and evaluating new product offerings before launch.

- Monitor your margin of safety monthly or quarterly as part of regular financial reviews, and recalculate immediately when making major business changes like price adjustments or product launches.

What is the margin of safety?

The margin of safety is the percentage by which your sales can fall before your business reaches its break-even point. This is where revenue equals costs and you make neither a profit nor a loss.

Think of it as your financial buffer against drops in demand or unexpected cost increases. The wider this margin, the more room you have to absorb setbacks without losing money.

What is the margin of safety formula?

The margin of safety formula is:

(Current sales − Break-even sales) ÷ Current sales = Margin of safety

This calculation gives you a percentage showing how much sales can drop before you start losing money. You can also use a net profit margin calculator to assess profitability.

Here's what each component means:

- Current sales: your total revenue from selling goods and services over a specific period

- Break-even sales: the exact revenue needed to cover all fixed and variable costs, where your business makes zero profit and zero loss

For example:

A business has current sales of $50,000 and needs $30,000 in sales to break even.

Margin of safety = ($50,000 − $30,000) ÷ $50,000 = 0.4 (40%)

This 40% margin means sales could drop by 40% before the business hits break-even. Any further drop would result in a loss.

How to calculate margin of safety

Follow these steps to calculate your margin of safety.

1. Find your current sales

Start by determining your current sales, whether actual figures or forecasts. You'll use this number as the starting point for your margin of safety calculation.

To find actual sales, pull your revenue figures from your POS system, ecommerce platform, or accounting software like Xero.

To find forecasted sales, use one or more of these methods:

- Analyse historical data: review past sales trends and seasonal patterns from your financial reports

- Conduct market research: study your target market, industry trends, and competitor performance

- Gather qualitative insights: ask your sales team or industry experts for their observations

- Apply quantitative methods: use statistical analysis on historical and market data to predict future sales

The best approach depends on your business type and the data you have.

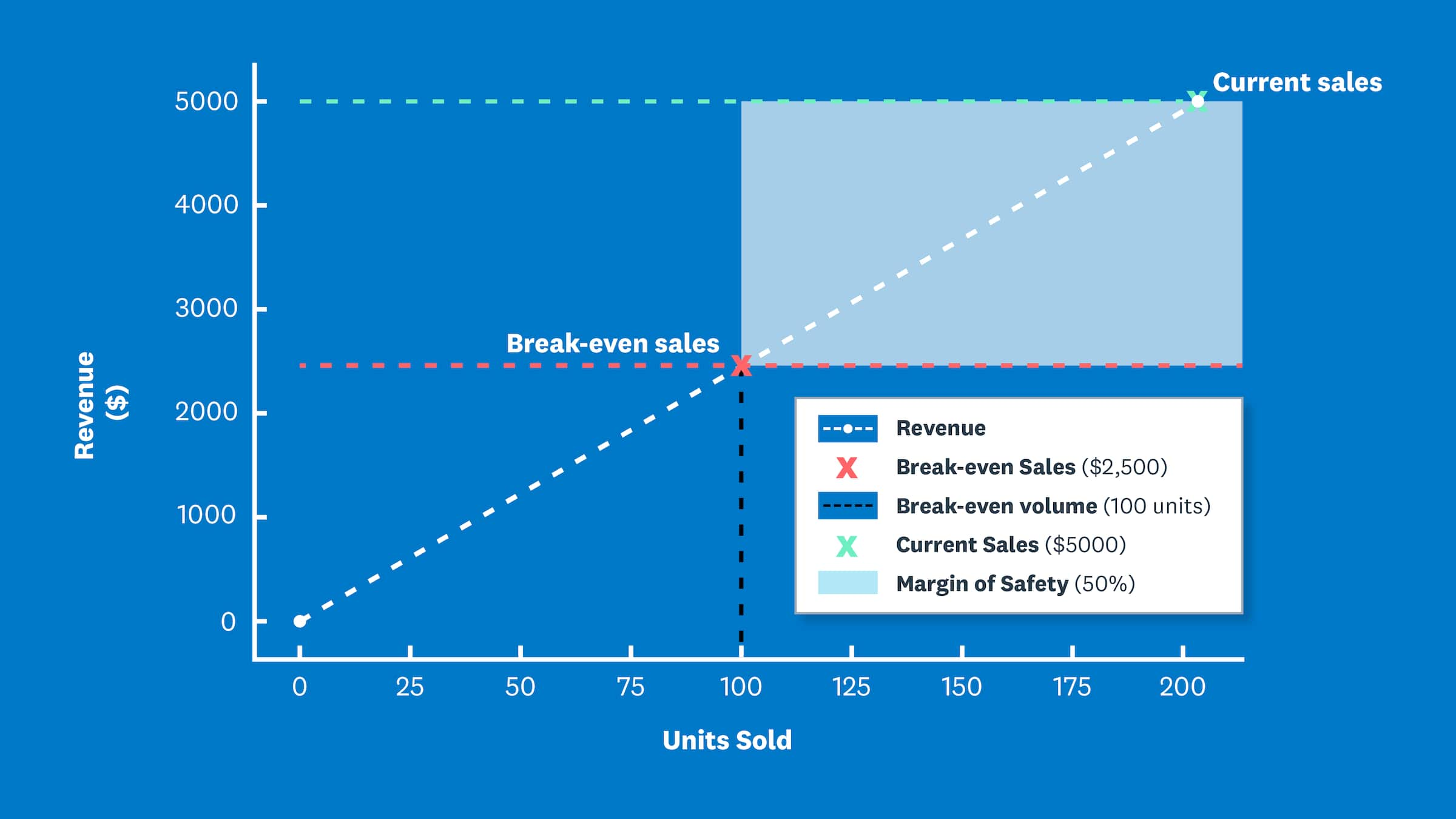

For example, a craft business uses a POS system to track monthly sales. Last month, sales were $5,000. This figure becomes the starting point for the margin of safety calculation in the steps below.

2. Calculate your break-even sales revenue point

For margin of safety calculations, you need your break-even sales revenue, not the number of units. Here's the formula:

Fixed costs ÷ ((Sales price − Variable cost) ÷ Sales price) = Break-even sales revenue

In this formula:

- Fixed costs: expenses that stay the same regardless of sales volume, such as salaries and rent

- Variable costs: expenses that change with sales volume, such as raw materials and sales commission

Learn more about variable costs and how they differ from fixed costs. Your accountant can also help you distinguish between them.

Say the craft business has:

- Fixed costs of $2,000

- Variable costs of $5 per unit

- A sales price of $25 per unit

Applying the formula:

2,000 ÷ ((25 − 5) ÷ 25) = 2,000 ÷ 0.8 = $2,500 break-even sales revenue

At a $25 sales price, the craft business needs $2,500 in revenue (100 units) to break even. This figure feeds into the final margin of safety calculation.

Learn more about the break-even point formula.

3. Apply the margin of safety formula

Apply the margin of safety formula to find your financial buffer:

(Current sales − Break-even sales) ÷ Current sales = Margin of safety

The result is your margin of safety ratio, the percentage by which sales can fall before your business starts operating at a loss.

Applying this to the craft business example, where current sales are $5,000 and break-even sales are $2,500:

($5,000 − $2,500) ÷ $5,000 = 50% margin of safety

This means the craft business could see sales drop by half before reaching break-even. A 50% margin represents a strong buffer, giving the owner room to absorb seasonal dips or unexpected cost increases.

What is a good margin of safety percentage?

Many businesses consider a margin of safety between 20% and 30% healthy, but the ideal buffer depends on your cost structure. For example, businesses with mostly variable costs might find 20% to 25% adequate, but those with high fixed costs may need a larger buffer. This gives you enough buffer to absorb unexpected drops in sales or increases in costs.

Here's how to interpret your results:

- Above 40%: strong buffer with significant room to absorb market shifts

- 20% to 40%: healthy margin with reasonable protection against downturns

- 10% to 20%: moderate risk, worth monitoring closely and planning improvements

- Below 10%: high risk, operating too close to break-even for comfort

Benchmarks vary by industry. Retailers with seasonal sales may need higher margins than service businesses with recurring revenue. Manufacturing businesses with high fixed costs often aim for larger buffers to offset their cost structure. For example, after one auto manufacturer invested in new machinery that increased fixed operating expenses, its resulting margin of safety of 5.8% highlighted how capital investments can tighten this financial cushion. Learn more about margin of safety calculations.

Why margin of safety matters for your small business

Margin of safety measures your business's financial resilience. It shows exactly how far sales can fall before you start making a loss.

- High margin (above 30%): lower risk, with room to absorb market shifts without disruption

- Low margin (below 15%): higher risk, operating close to break-even with limited flexibility

Consider how an external shock would affect your business. For example, if supplier prices rise by 10%, your variable costs increase, pushing up your break-even point.

This eats into your margin of safety and leaves you more exposed to further cost increases or falling sales.

Your margin of safety also supports smarter financial decisions across your business.

How to use margin of safety in business decisions

Your margin of safety guides decisions across key areas of your business:

- Setting performance targets: calculate your break-even point to set achievable sales goals that keep you profitable

- Adjusting prices: review pricing when margins shrink to ensure each sale covers costs adequately

- Controlling costs: treat a low margin as a signal to reduce expenses and protect your buffer

- Evaluating new offerings: assess how proposed products or services affect your margin before launching

Using margin of safety with other financial metrics

Margin of safety works best alongside other financial metrics. When combined with cost-volume-profit (CVP) analysis, margin of safety gives you a clearer view of both profitability and risk than either metric alone. Learn more about profitability ratios. One study on U.S. manufacturing firms found that companies using CVP models demonstrate better responsiveness to market shifts and cost fluctuations.

Cost-volume-profit (CVP) analysis models how changes to your cost structure, sales volume, and pricing affect profitability. While margin of safety shows your current buffer, CVP helps you plan by testing different scenarios. For instance, a study of Sri Lankan companies found a positive correlation between using CVP and enhanced decision-making efficiency.

Track your margin of safety with Xero

Understanding your margin of safety helps you spot financial risk early, set realistic targets, and make confident decisions about pricing, costs, and growth.

Xero simplifies the process by giving you quick access to the financial data and reports you need. Instead of tracking down figures and updating spreadsheets manually, you can calculate your margin of safety faster and monitor it over time.

Get one month free and see how Xero helps you stay on top of your business finances.

FAQs on margin of safety

Here are answers to common questions about calculating and using your margin of safety.

What is a good margin of safety percentage?

A margin between 20% and 30% is generally healthy, though this varies by industry and business model. Aim for a buffer that lets you absorb unexpected sales drops without immediately losing money.

What does a 50% margin of safety mean?

A 50% margin of safety means your sales could drop by half before your business reaches its break-even point. This represents a strong financial buffer with significant room to absorb market shifts.

What should I do if my margin of safety is low?

Focus on increasing revenue, reducing costs, or both. Review your pricing strategy, cut unnecessary expenses, diversify your income streams, or boost sales volume to widen your buffer.

How often should I calculate margin of safety?

Calculate it monthly or quarterly as part of your regular financial review. Also recalculate when making major decisions like launching new products, adjusting prices, or planning expansion.

Can margin of safety be negative?

Yes. A negative margin means you need to take action to reach your break-even point and return to profitability. This requires immediate action to reduce costs, increase prices, or boost sales volume.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.