Cash flow projection: how to create, read and use it

Learn how cash flow projection helps you plan, avoid shortfalls, and grow with confidence.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 30 March 2026

Table of contents

Key takeaways

- Create cash flow projections by calculating your opening balance, estimating cash inflows and outflows, then determining your net cash flow to identify potential shortages before they happen.

- Update your cash flow projection at least monthly to maintain accuracy, as estimates become less reliable the further into the future you project.

- Use historical data from past bank statements and accounting records to identify typical income and expense patterns, and build in a buffer for late payments and unexpected costs.

- Compare your projections to actual results each month to spot patterns and improve your forecasting accuracy over time.

What is a cash flow projection?

A cash flow projection is a forecast of your expected cash inflows and outflows over a set period. It shows how much money you'll have available at any point in the future, helping you plan spending and spot potential shortages before they happen.

A cash flow projection differs from a cash flow statement. A statement records past cash movements, while a projection estimates future ones.

Cash flow projection vs cash flow forecast

The terms "cash flow projection" and "cash flow forecast" are often used interchangeably. Both estimate future cash inflows and outflows to help you plan ahead.

Some businesses use "projection" for shorter-term estimates (days or weeks) and "forecast" for longer-term planning (months or years). In practice, the distinction matters less than the habit of regularly estimating your future cash position.

Cash flow projection vs cash flow statement

A cash flow projection estimates future cash movements based on expected transactions. A cash flow statement records actual cash movements that have already occurred.

Use projections to plan ahead. Use statements to review past performance and verify your projections were accurate.

Cash flow forecast vs cash flow statement

A cash flow forecast predicts where your cash will be in the future. A cash flow statement shows where your cash has been.

Both are valuable. Forecasts help you prepare for what's coming. Statements help you understand what happened and improve future forecasts.

Why is a cash flow projection important?

Cash flow projections help you avoid running out of money. When you know what's coming in and going out, you can pay bills on time, cover payroll, and pay yourself.

As costs rise, accurate cash flow management becomes even more critical. Research shows that forecasting is difficult, with an EY-Parthenon analysis finding that only 28% of companies' cash forecasts were within 10% of their annual targets. A projection gives you the visibility you need to stay ahead.

Benefits of a cash flow projection

Cash flow projection is a good financial habit to get into. It has multiple operational and financial benefits for your business, including:

- Spotting cash shortages early: gives you time to delay spending, request supplier credit, or secure a business loan

- Assessing growth affordability: shows whether you can afford new tools, equipment, or an additional employee

- Protecting your own pay: ensures you have enough cash to pay yourself as the business owner

- Tracking financial trends: reveals quickly if expenses are climbing or income is slumping

- Identifying fixable problems: highlights issues like slow-paying customers, impractical payment terms, or seasonal cash cycles. For example, by improving its forecasting, one company identified issues with its inventory and accounts that unlocked potential savings of up to $610 million.

What are the key components of a cash flow projection?

Your cash flow projection includes five key components:

- Opening balance: the amount of cash in your bank at the start of the period

- Cash inflows: money coming in, typically from sales but also from loans, grants, or asset sales

- Cash outflows: money going out for expenses, wages, taxes, and other costs

- Net cash flow: the difference between inflows and outflows, showing whether your cash reserves grew or shrank

- Closing balance: the amount of cash remaining at the end of the period, which becomes your next period's opening balance

Types of cash flow forecasts

Different forecasting approaches suit different business needs. Choose the method that matches your planning horizon and the level of detail you require.

Short-term vs long-term cash flow projections

The timeframe of your projection affects how you use it:

- Short-term projections cover days or weeks, typically 13 weeks or less. Use them to manage immediate cash needs, like making payroll or paying suppliers.

- Long-term projections cover months or years. Use them to plan for growth, assess loan affordability, or prepare for seasonal fluctuations.

Most small businesses benefit from both: a short-term projection for day-to-day decisions and a longer-term view for strategic planning.

Direct vs indirect cash flow forecasting methods

Two main methods exist for creating cash flow forecasts:

- Direct method: lists actual expected cash receipts and payments. This approach is simpler and works well for short-term projections.

- Indirect method: starts with net income and adjusts for non-cash items and changes in working capital. This approach is more complex but useful for longer-term planning.

For most small businesses, the direct method is easier to create and understand.

How to create a cash flow projection

Creating a cash flow projection involves estimating when money will come in and go out, then calculating how those transactions affect your cash position over time.

You can build a projection using a spreadsheet or accounting software. Here's how to get started.

Follow these four steps to create your projection:

1. Calculate your opening cash balance

Start with the amount of cash you have in the bank at the beginning of the period you're forecasting for.

2. Estimate your cash inflows

List all the cash you expect to receive during the period. This includes payments from customers, tax refunds, or loan money.

3. Project your cash outflows

List all the cash you expect to spend. Include regular bills, payroll, rent, and less frequent costs like taxes or equipment repairs.

4. Calculate net cash flow and closing balance

Subtract your total cash outflows from your total cash inflows to get your net cash flow. Add the net cash flow to your opening balance to find your closing balance for the period.

Tips for creating accurate cash flow projections

Accurate projections require realistic estimates and regular updates. Follow these practices to improve your forecasting:

- Use historical data: Review past bank statements and accounting records to identify typical income and expense patterns

- Account for timing: Record transactions when cash actually moves, not when invoices are sent or received

- Include irregular expenses: Add annual fees, tax payments, and seasonal costs that don't appear every month

- Build in a buffer: Assume some customers will pay late and some expenses will arrive earlier than expected

- Review and adjust: Compare projections to actual results monthly and refine your estimates based on what you learn

Example of a cash flow projection

The finance manager of Tiny Construction wants to assess whether the business can afford a $20,000 equipment purchase next month.

Starting position:

- Opening balance: $45,000

- Expected cash inflows: $90,000 from outstanding invoices and sales forecasts

- Other income: none expected this month

So the "money in" part of the cash flow projection will look like this:

The "money out" part of the cash flow projection will look like this:

The 'net cash flow' and 'closing balance' will be shown here.

Calculating the result:

- Net cash flow: $90,000 inflows minus $65,000 outflows equals $25,000

- Closing balance: $45,000 opening balance plus $25,000 net cash flow equals $70,000

With $70,000 available at month end, Tiny Construction can afford the $20,000 equipment purchase and still have $50,000 as their opening balance for the following month.

This example shows how cash flow projections help you make investment decisions. You can see whether you can afford a purchase outright or need to consider financing.

Tools and software for cash flow projections

Accounting software can generate cash flow projections automatically by pulling data from your existing transactions. This saves time and reduces manual errors.

Here are some options:

- Xero: Tracks your incomings and outgoings, then creates a projection with a few clicks

- Forecasting apps: Tools like Spotlight, Fathom, and Calxa integrate with Xero to provide longer-term, more detailed projections

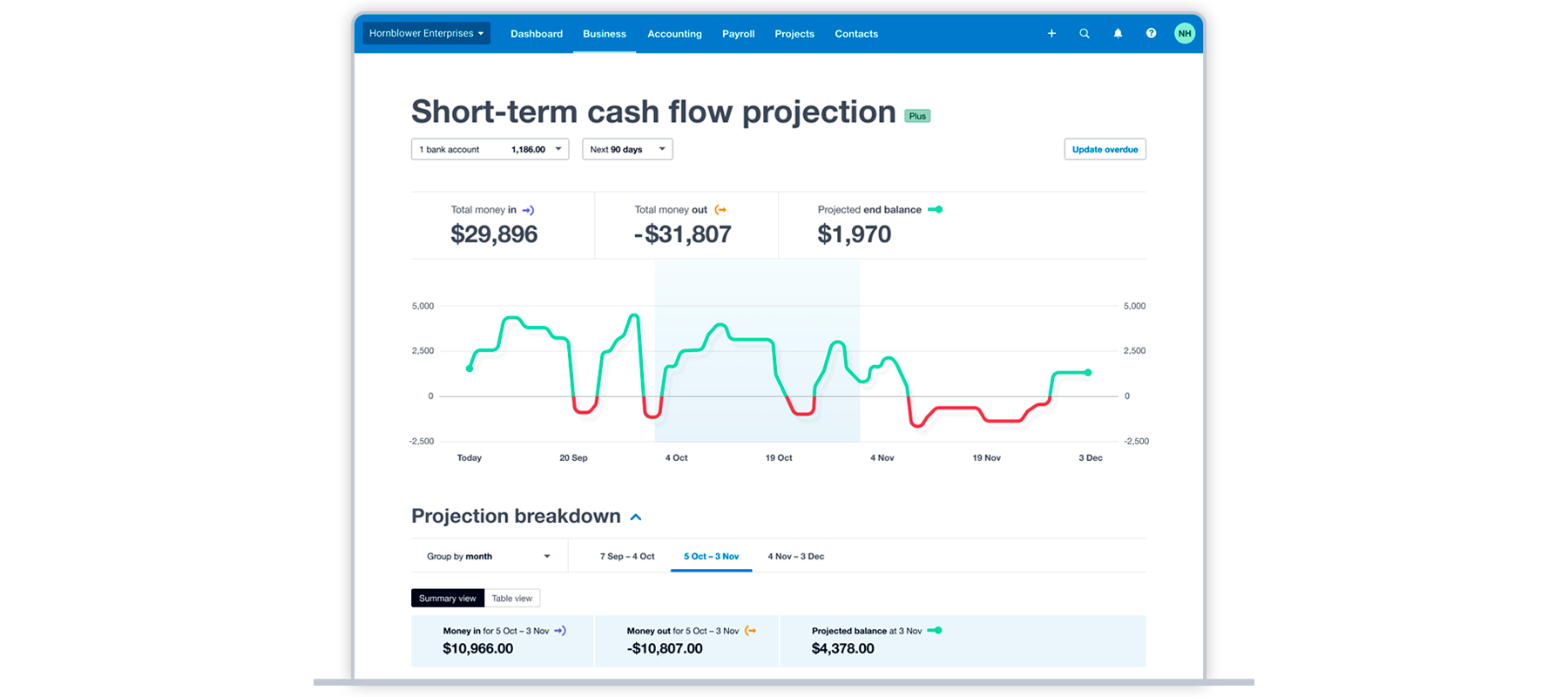

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

Using software means your projection updates as new transactions come in, giving you a real-time view of your cash position.

How to read and analyze your cash flow projection

Reading your cash flow projection means checking three key figures to understand your financial position:

- Closing balance: The cash you expect to have at the end of each period. A positive balance means you can cover upcoming expenses.

- Net cash flow: The change in your cash reserves during the period. A negative number means you spent more than you received.

- Accuracy: Compare your projection to actual results. Note where you overestimated or underestimated, and adjust future projections accordingly.

Reviewing accuracy regularly helps you spot patterns and improve your forecasting over time. Some companies with good processes achieve up to an estimated 90% quarterly accuracy.

How often should you update your cash flow projection?

Update your cash flow projection at least monthly, or more frequently if your business has variable income or expenses.

The further into the future you project, the less accurate your estimates become. Regular updates keep your projection useful.

For a rolling 12-month projection, refresh at the end of each month. Drop the completed month, add a new month at the end, and review your estimates for the months in between.

Simplify cash flow forecasting with Xero

Cash flow projection gives you the visibility you need to make confident decisions about your business. Whether you're planning for growth or managing tight margins, knowing what's coming helps you stay in control.

With Xero, cash flow forecasting becomes simple. Your transactions sync automatically, and you can generate projections with a few clicks instead of building spreadsheets from scratch. Try Xero free for one month and see how much easier cash flow planning can be.

FAQs on cash flow projection

Here are answers to common questions about cash flow projections for small businesses.

What's the difference between a cash flow projection and a cash flow forecast?

The terms are often used interchangeably. Both estimate future cash inflows and outflows to help you plan spending and avoid shortages.

How far into the future should my cash flow projection go?

Most small businesses project 12 months ahead, with weekly or monthly detail. Shorter projections (four to eight weeks) work well for day-to-day cash management.

Can I create a cash flow projection without accounting software?

Yes. You can build a projection using a spreadsheet by listing expected inflows and outflows, then calculating your running balance. Software makes the process faster and reduces manual errors.

What should I do if my projection shows I'll run out of cash?

Act early. Options include delaying non-essential spending, chasing overdue invoices, negotiating longer payment terms with suppliers, or arranging a line of credit before you need it.

How can I improve the accuracy of my cash flow projections over time?

Compare your projections to actual results each month. Note where estimates were off, identify patterns, and adjust future projections based on what you learn.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.