Financial statements: types, how to read and use them

Learn how financial statements drive smarter decisions, steady cash flow, and funding wins for your small business.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Thursday 5 March 2026

Table of contents

Key takeaways

- Prepare your three core financial statements monthly or quarterly to track your business's financial health, focusing on the balance sheet (what you own versus owe), income statement (revenue minus expenses), and cash flow statement (money moving in and out).

- Use financial ratios like the current ratio and quick ratio to assess whether you can cover short-term obligations, aiming for a quick ratio between 1.0 and 1.5 to maintain healthy liquidity.

- Analyse all three statements together rather than focusing solely on profit, as a business can show profit on paper while struggling with cash flow issues that prevent paying bills and payroll.

- Compare financial statements across multiple periods to identify trends in revenue, expenses, and cash flow, which helps you spot opportunities for growth and areas needing improvement.

What is a financial statement?

A financial statement is a formal report that summarises your business's financial activities and how it has performed over a specific period. Lenders and investors use financial statements to assess your business's financial health and earnings potential.

Financial statements typically cover a month or quarter, and according to international standards, businesses must present a complete set of financial statements at least annually.

Types of financial statements

There are four main types of financial statements that give you a complete picture of your business's financial health:

- Balance sheet: Shows what you own and owe at a point in time

- Income statement: Tracks revenue and expenses over a period

- Cash flow statement: Records money moving in and out of your business

- Statement of changes in equity: Shows how retained earnings change over time

The first three are the most commonly used by small businesses.

Balance sheet

A balance sheet is a snapshot of your business's financial condition at a specific point in time. It compares what you own (assets) with what you owe (liabilities).

- Assets: Machinery, equipment, patents, intellectual property, and cash

- Liabilities: Long-term debts, accounts payable, and loans

The difference between assets and liabilities is your business's equity, which is often used as a starting point for valuing a business.

To find the equity, use the formula shown in the image above.

This formula helps you evaluate your business's financial stability.

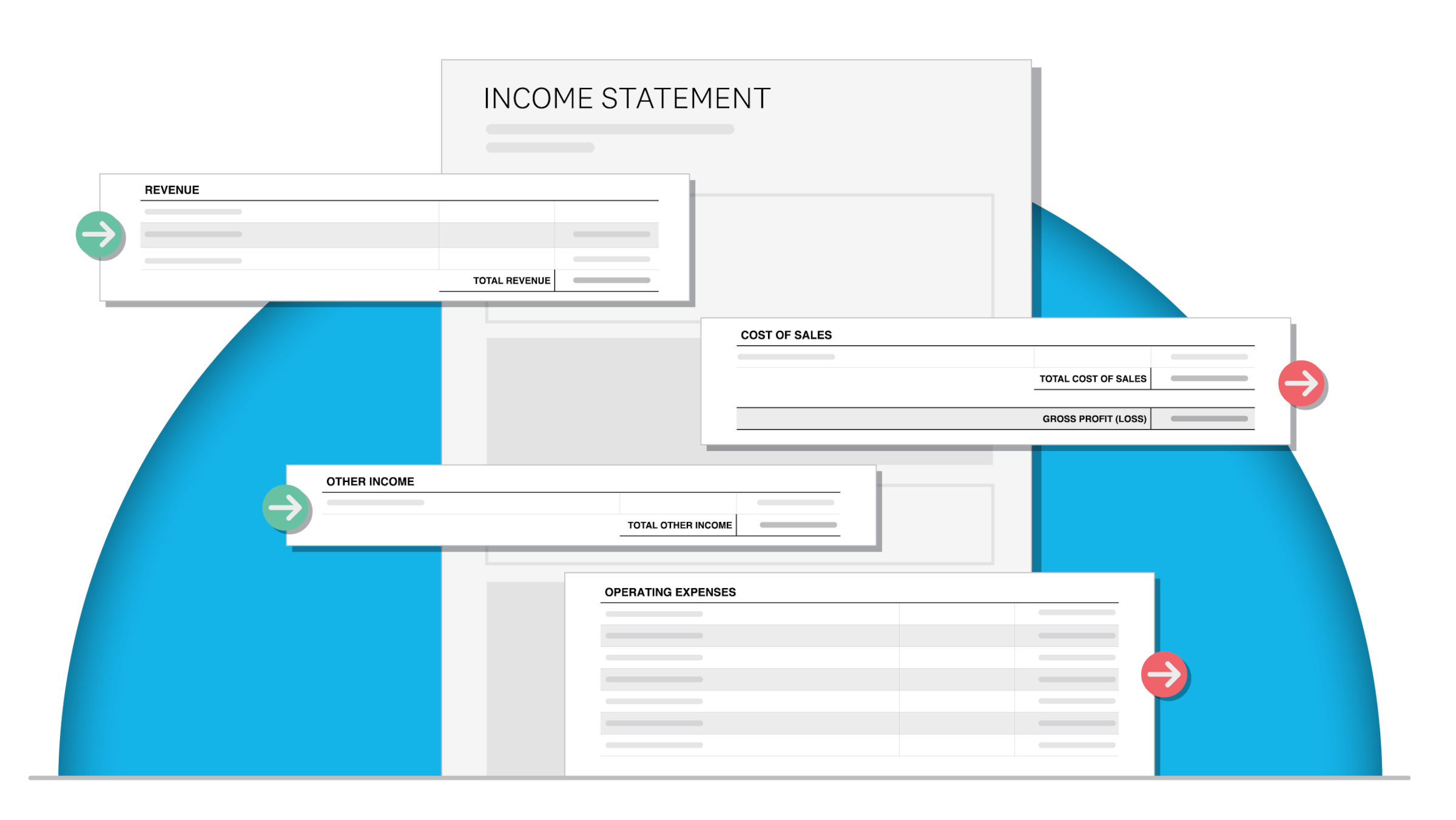

Income statement/Profit and loss statement

An income statement (also called a profit and loss statement) shows your business's revenues and expenses over a specific period. Subtract expenses from revenues to calculate your net income.

Here's an example for a manufacturing business:

- Revenue: $150,000

- Operating expenses: $50,000 (office hire, utilities)

- Cost of sales: $70,000 (materials, labour)

- Net income: $30,000

This tells you whether your business is profitable and where your money is going.

Cash flow statement

A cash flow statement shows how cash moves in and out of your business over a specific period. It tells you whether you can cover short-term expenses like bills and payroll.

Cash flow statements track three types of activity:

- Operating activities: Cash from customer sales and day-to-day business operations

- Investing activities: Purchases and sales of assets like machinery or equipment

- Financing activities: Money from loans, investments, or dividends

Statement of changes in equity

A statement of changes in equity (also called a retained earnings statement) shows how much profit your business keeps after paying all costs, including dividends to shareholders or owners.

Businesses typically retain earnings to:

- repay debt

- reinvest in growth

- build a cash reserve for unexpected expenses

This statement helps demonstrate your business's growth potential to investors and lenders.

How to create financial statements

Creating accurate financial statements doesn't require an accounting degree. Here's what you need to get started.

1. Gather your financial records

Before creating any financial statement, collect these essential records:

- Bank statements: All business account transactions for the period

- Invoices: Both issued to customers and received from suppliers

- Receipts: For all business expenses

- Payroll records: Wages, taxes, and superannuation payments

- Loan documents: Balances and payment schedules

Keep these records organised by date and category to make statement preparation faster.

2. Choose your preparation method

You have three main options for creating financial statements:

- DIY with templates: Use spreadsheet templates for basic statements (best for very small businesses with simple finances)

- Accounting software: Platforms like Xero automatically generate statements from your transaction data (best for most small businesses)

- Hire an accountant: Work with a professional for complex situations or when you need certified statements for lenders

Most small businesses find accounting software strikes the right balance between cost and accuracy.

3. Best practices for preparing accurate statements

Follow these best practices for accuracy:

- Mixing personal and business expenses: Keep accounts separate to ensure accurate reporting

- Recording revenue before it's earned: Only count sales when goods or services are delivered

- Forgetting to reconcile accounts: Match your records to bank statements monthly

- Using inconsistent time periods: Compare like with like when analysing trends

- Ignoring accounts receivable: Unpaid invoices affect both your income statement and cash flow

Why financial statements are important for small businesses

Financial statements help you make smarter business decisions by giving you a clear view of your business's financial health. When you understand your financial statements, you can spot opportunities early, identify growth areas, and plan for success.

Here's what financial statements help you do:

- Assess financial health: See your profitability, cash flow, and equity at a glance to make stronger financial decisions

- Attract investors and secure loans: Show lenders and investors that your business is profitable and can repay debts

- Comply with tax requirements: Meet reporting rules and tax obligations with confidence

- Track business performance: Spot trends over time and identify which products or areas need attention

- Manage cash flow: Plan for expenses, payroll, and unexpected costs

- Make informed decisions: Use accurate data to guide business growth

How to use financial statements to analyse your business

Each type of financial statement serves a specific purpose. Here's how to use them to analyse your business and make better decisions.

Analyse financial performance with the income statement

Your income statement helps you understand profitability. Use it to:

- Evaluate profitability: Compare total revenue against net income to see if your business is making money

- Monitor expenses: Identify where you're overspending by reviewing cost of goods sold and operating expenses

- Track growth trends: Compare statements from different periods to spot changes in revenue, costs, and profit margins

The income statement provides the data you need to calculate three key profitability metrics:

- Gross profit: Revenue minus cost of goods sold

- Operating income: Gross profit minus operating expenses

- Net income: Your final profit after all expenses

These calculations show whether you need to adjust prices or reduce costs.

Manage assets and plan for growth with the balance sheet

Your balance sheet helps you understand your business's financial position. Use it to:

- Assess liquidity: Compare current assets to current liabilities to see if you can cover short-term obligations

- Evaluate solvency: Examine long-term liabilities and equity to gauge financial stability (a balanced debt-to-equity ratio supports financial stability)

- Track asset management: Review how efficiently assets like inventory, property, and equipment contribute to revenue

Your balance sheet provides the numbers you need to calculate liquidity ratios that show whether you have enough cash to pay your bills.

The cash ratio liquidity formula helps you figure out if you have enough cash to cover payroll, expenses, and loan payments in the coming year.

-calculation-2.1708626946541.png)

The quick ratio measures whether you can cover your core costs over the next three months. While expectations vary by industry, the sweet spot for a healthy quick ratio often falls between 1.0 and 1.5.

The current ratio formula, unlike the quick ratio, includes your business's inventory value (from your balance sheet). According to financial analysts, a wide gap between the two ratios can signal a heavy reliance on inventory to meet short-term obligations.

Manage your cash flow with the cash flow statement

Strong cash flow means your business can meet its financial obligations. Your cash flow statement reveals whether you're generating enough cash to cover expenses, and where adjustments might be needed.

Use the cash flow statement to:

- Analyse operating cash flow: Check if your core business activities generate enough cash to sustain operations (positive cash flow confirms your core business activities are sustainable, even when profits look healthy)

- Judge investment quality: Track how much cash goes toward equipment or expansion to see if you're reinvesting for growth

- Monitor financing activities: Review cash from loans, equity financing, or dividends to understand how external funding affects your cash position

Analyse growth with the retained earnings statement

The retained earnings statement shows how your business handles its profits over time. Use it to assess:

- Growth potential: Growing retained earnings suggest your business can reinvest in itself without borrowing

- Financial health: Declining retained earnings may indicate profits are being used to cover losses or debts, which suggests reviewing your profit allocation strategy

Ways to use your financial statements

Consider the big picture – not just profit

Looking at all your financial statements together gives you a complete picture of your business health. Analysts consider earnings to be of high quality only when cash from operating activities is higher than net income.

Review all three main statements together, including the income statement, balance sheet, and cash flow statement, to get a complete picture of your financial health.

Pay attention to your cash flow

Profitability and cash flow work together to keep your business healthy. Check your cash flow statement regularly to track liquidity and make sure you can cover short-term costs like payroll and bills.

Know the difference between revenue and cash

Revenue isn't the same as cash. A sale recorded on your income statement may not have reached your bank account yet.

Track accounts receivable separately so you always know how much cash you actually have available to spend.

Analyse trends by comparing your financial statements

Compare financial statements across multiple periods to identify patterns in revenue, expenses, and liabilities. Official accounting frameworks require comparative information to help users assess changes and trends.

This helps you invest in areas that are performing well and identify opportunities for improvement.

Get across your financial ratios

Financial ratios turn your statement data into actionable insights about liquidity, profitability, and overall financial health.

Key ratios to track include:

- Current ratio: Measures ability to pay short-term obligations

- Quick ratio: Measures liquidity without counting inventory

- Debt-to-equity ratio: Shows how much debt you're using compared to equity

Financial statement templates for your business

Pre-made templates make creating financial statements faster and more consistent. Use them to build balance sheets, income statements, and cash flow statements without starting from scratch each time.

Download Xero's free financial statement templates to get started.

Streamline your financial statements with Xero

Understanding your financial statements gives your business a better chance of success, which is critical when only about one in three small businesses typically reach their 10-year mark. Xero accounting software automates financial reporting, provides real-time insights, and integrates payroll and invoicing, so you can focus on running your business.

Get one month free and see how easy financial management can be.

FAQs on financial statements

Still have questions about financial statements? Here are answers to some common concerns.

What's the difference between the income statement and cash flow statement?

The income statement shows whether your business is profitable by tracking revenue and expenses. The cash flow statement shows whether you have enough cash to pay your bills by tracking money moving in and out.

A business can be profitable on paper, so tracking cash flow helps you stay prepared when customers pay on different schedules.

Does my small business need all four types of financial statements?

Most small businesses need three statements: the balance sheet, income statement, and cash flow statement. These cover the essentials of financial health.

The retained earnings statement is useful if you're planning to reinvest profits in growth or pay off debt.

How often should I prepare financial statements?

Prepare financial statements monthly or quarterly for the best visibility into your business. Annual statements are the minimum for tax compliance, but more frequent reporting helps you spot trends and opportunities faster.

Can I automate my financial statements?

Yes. Accounting software like Xero automatically generates financial statements from your transaction data. This saves time, improves accuracy, and keeps your records ready for tax time.

What financial statements do lenders require for a business loan?

Most lenders require three statements: a balance sheet, income statement, and cash flow statement. They typically want to see at least two years of historical data, plus year-to-date figures. Some lenders also request tax returns and accounts receivable/payable ageing reports.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.