Australia Small Business Insights

This analysis focuses on core performance metrics of sales growth, jobs growth, wages growth, late payments and time to be paid.

Positive momentum at risk from fuel shock

Published: 30 April 2026

The latest Xero Small Business Insights (XSBI) data for Australia shows small businesses had a solid start to the year. Sales (+7.2% year-on-year), jobs (+3.4% y/y) and wages (+2.7% y/y) are now within touching distance of their historical average growth rates. Unfortunately this momentum is at risk due to events in the Middle East, which have pushed up fuel prices, adding to already building domestic inflation pressure.

Sales in small businesses grew 7.2% year-on-year (y/y) in the March quarter, similar to the 7.3% y/y rise in the December quarter. Sales are now growing only just below the historical average for this series of 7.9% y/y. Breaking down the monthly movements over the quarter, sales rose 4.6% y/y in January, 6.0% y/y in February and surged 10.9% y/y in March. The outcomes for the latter two months are particularly positive given the Reserve Bank of Australia increased the cash rate in both these months, which could have negatively impacted sales.

The monthly March data is an early insight into how small businesses are being impacted by the fuel price spike caused by the conflict in the Middle East. XSBI sales are measured in nominal terms, which includes changes in both sales volumes and prices. CPI data helps to understand how much of the March sales rise is due to prices and how much is due to higher volumes. Is the CPI showing broad based price increases or isolated to spikes in fuel prices? At the time of finalising this report, the CPI data for March had not yet been released by the ABS. Nevertheless, the March CPI reports from other countries, such as the US, UK and Canada, have all shown that price increases to date are largely in fuel only and not broad based. This suggests the latest month of XSBI sales growth is most likely reflecting a genuine improvement in activity rather than being due to higher prices.

The lack of evidence of widespread price impacts in XSBI sales is also supported by industry data. The transport and logistics industry - which is most directly exposed to the fuel price surge - had a 13.2% y/y rise in sales in the month of March. This was 8.2 percentage points higher than sales in February, which was the largest above-average month-to-month change of all industries tracked by XSBI. This further supports the idea that, so far at least, price increases are not widespread amongst small businesses and that the rise in sales in March is more likely due to increases in physical sales than prices.

.1777041188675.png)

Looking at the quarter overall, strong sales performances were recorded by construction (+10.4% y/y), healthcare (+9.2% y/y) and financial services (8.8% y/y). Those sectors that are more interest rate sensitive were a little below the national result - arts and recreation (+5.5% y/y) and hospitality (5.1% y/y). The best performing states in terms of sales were Queensland (+9.8% y/y) and Western Australia (+8.1% y/y).

This data is an early insight into how small businesses are being impacted by the Middle East conflict.

XSBI Australia January 2026 - March 2026 data

As sales growth has gathered momentum, so too has jobs growth. Jobs grew 3.4% y/y in the March quarter, after a 2.8% y/y increase in the December quarter. Public administration (+5.6% y/y) led the gains, with construction (+5.3% y/y) continuing to be a strong performer. Hospitality (+0.7% y/y) and administrative services (+1.3% y/y) remained the softest industries for jobs growth. As with sales, the best performing states were Western Australia (4.5% y/y) and Queensland (4.1% y/y).

.1777041186752.png)

Wages rose 2.7% in the March quarter, up slightly from 2.5% y/y in the December quarter. This quarterly result is only just below the historical average (+2.9% y/y) reflecting increasingly tight conditions in hiring. Hospitality workers had the largest pay increase in the past year (+3.5% y/y), although this had little impact attracting new workers to the sector. Construction was also solid, with wages up 3.3% y/y. Most other industries were around the national average, with the exception of transport and logistics (+2.1% y/y) and information, media and telecommunications (+2.2% y/y).

.1777041192038.png)

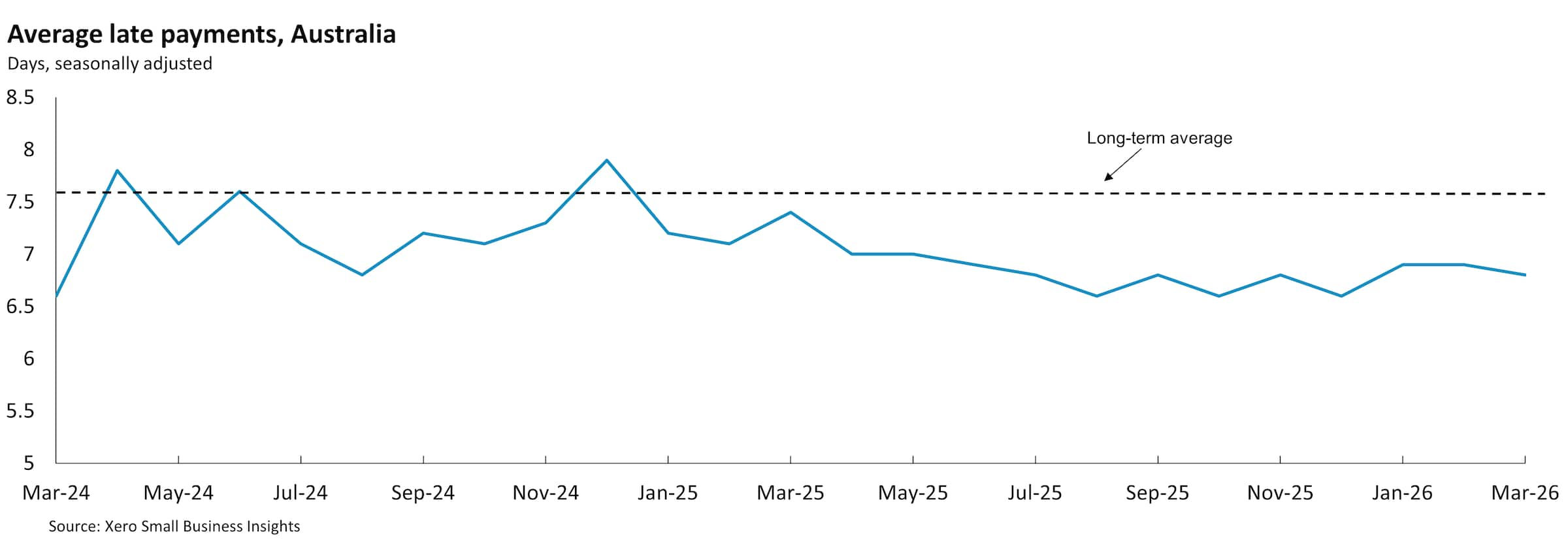

Both payment time metrics held on to recent improvements in these series. The average length of time small businesses waited to be paid, after issuing an invoice, was 24.1 days - similar to the December quarter (24.0 days). Small businesses were paid, on average, 6.9 days late in the March quarter, only slightly longer than the 6.7 days late of the previous quarter.

.1777041189706.png)

Overall, small businesses had a solid start to 2026 despite two interest rate hikes during this period.

Looking ahead, the impact of higher fuel prices is the main risk to the outlook, coupled with mounting concerns about fuel availability. This external shock has come at a frustrating time for small businesses, just as sales growth was returning to historical averages. This sudden price spike hurts small businesses both directly, through rising costs of fuel (and eventually many other inputs), and indirectly, as customers are left with less to spend on non-fuel goods and services. Importantly, it is still early days in this crisis and the fuel price impacts have not yet worked through the economy. To date much of the price impacts are only in heavily fuel-exposed industries, such as transport and logistics. However, business profit margins can't absorb these dramatically higher fuel prices indefinitely. These rising transport costs are likely to increasingly flow through to the price of goods and services across many industries in the coming months, spreading the economic damage and further squeezing household budgets.

Fuel prices are unlikely to come down meaningfully any time soon, given it will take many months for the world oil market to return to 'normal', even after the Strait of Hormuz is reopened. In addition, the longer fuel prices remain high the greater the risk that the Reserve Bank of Australia will respond with more increases in the cash rate to combat the widening inflation shock. As a country dependent on fuel imports, the risk of actual fuel shortages rises the longer hostilities continue in the Middle East. Current advice is that fuel stocks are sufficient and small businesses should continue to buy and use fuel as normal. The Australian Government is working to secure future supply, given an inability to access fuel would clearly have a bigger negative impact on the country than the price hikes have to date.

During periods of major geopolitical upheaval that are outside their control, small business owners need to continue to focus on the aspects of their business they can influence - such as managing cash flow, using prompt payment practices and delivering great customer service.

For more information on the XSBI metrics, see our methodology page.

Disclaimer

This report was prepared using Xero Small Business Insights data and publicly available data for the purpose of informing and developing policies to support small businesses.

This report includes and is in parts based on assumptions or estimates. It contains general information only and should not be taken as taxation, financial, investment or legal advice. Xero recommends that readers always obtain specific and detailed professional advice about any business decision.

The insights in this report were created from the data that was available as at the date it was extracted. Data used was anonymised and aggregated to ensure individual businesses can not be identified.

Find out more about XSBI

If you have any questions about Xero Small Business Insights, reach out to us.