NOPAT: definition, formula and calculation with example

Learn how net operating profit after tax (NOPAT) reveals true operating profit and helps you make better decisions.

Written by Kari Brummond—Content Writer, Accountant, IRS Enrolled Agent. Read Kari's full bio

Published Friday 20 February 2026

Table of contents

Key takeaways

- Calculate NOPAT using the formula Operating Profit × (1 − Tax Rate) to measure your business's true operational performance after taxes but before interest expenses.

- Use NOPAT to make fair comparisons between businesses with different debt levels, as it excludes financing costs and focuses purely on operational efficiency.

- Apply NOPAT as the foundation for calculating Economic Value Added (EVA) and return on invested capital (ROIC) to determine if your business creates value beyond its cost of capital.

- Track NOPAT quarterly or annually to monitor operational performance trends and guide capital allocation decisions separate from financing arrangements.

What is NOPAT?

Now let's explore what NOPAT is and how it works.

Net Operating Profit After Tax (NOPAT) measures how much profit your business earns from its core operations after paying taxes, but before accounting for interest expenses. Unlike net income, NOPAT excludes financing costs and non-operating income, giving you a clearer picture of operational performance.

NOPAT focuses exclusively on core business performance. Here's what it includes and excludes:

What NOPAT includes:

- revenue from primary business operations

- operating expenses (salaries, rent, supplies)

- tax obligations on operating income

What NOPAT excludes:

- interest expenses on loans, credit cards, or other debt

- investment gains or losses (such as stock holdings)

- non-operating income (rental income, one-time sales)

This focus makes NOPAT useful for calculating returns on invested capital and comparing businesses with different financing structures.

Why is NOPAT important?

NOPAT reveals operational profitability independent of financing decisions. Because it excludes interest expenses, you can compare businesses with different debt levels on equal footing. This makes NOPAT essential for:

- comparing companies across industries or regions

- evaluating how efficiently a business uses invested capital

- calculating Economic Value Added (EVA) and return on invested capital (ROIC)

Reveals true business performance

NOPAT isolates operational performance from financing decisions. By excluding interest expenses while including taxes, you see how the business performs based purely on its operations.

This clarity is especially valuable when:

- evaluating businesses with complex capital structures

- comparing companies with multiple investors or debt arrangements

- identifying operational improvements separate from financing optimisations

Helps to standardise comparisons

NOPAT creates equal comparisons by removing financing differences between businesses.

Example: Comparing two acquisition targets

Company A:

- Net profit: $100,000

- Interest expenses: 0

- NOPAT: $100,000

Company B:

- Net profit: $80,000

- Interest expenses: $40,000

- NOPAT: $120,000

At first glance, Company A looks more profitable. But Company B's lower net profit reflects its debt burden, not weaker operations. NOPAT reveals Company B actually generates stronger operational earnings, confirming that when comparing companies with the same operating profit, the NOPAT value is equivalent regardless of debt.

This comparison also works across tax jurisdictions, showing exactly how different tax rates affect operational profitability.

Improved decision-making

NOPAT is essential for calculating Economic Value Added (EVA), which measures whether a business creates value beyond its cost of capital.

EVA formula:EVA = NOPAT − (Invested Capital × Cost of Capital)

Example calculation:

- NOPAT: $50,000

- Invested capital: $200,000 (comprising $100,000 in loans at 6% and $100,000 in equity)

- Weighted average cost of capital: 3%

- Capital charge: $200,000 × 3% = $6,000

- EVA: $50,000 − $6,000 = $44,000

This $44,000 represents the true value created above what investors require as a minimum return. EVA helps you assess whether investments are generating adequate returns and guides decisions about future capital allocation, as its value can fluctuate significantly year to year. For example, one company's EVA was $2,805, $1,187, and negative $347 across three consecutive years.

For more details, see these EVA calculation examples.

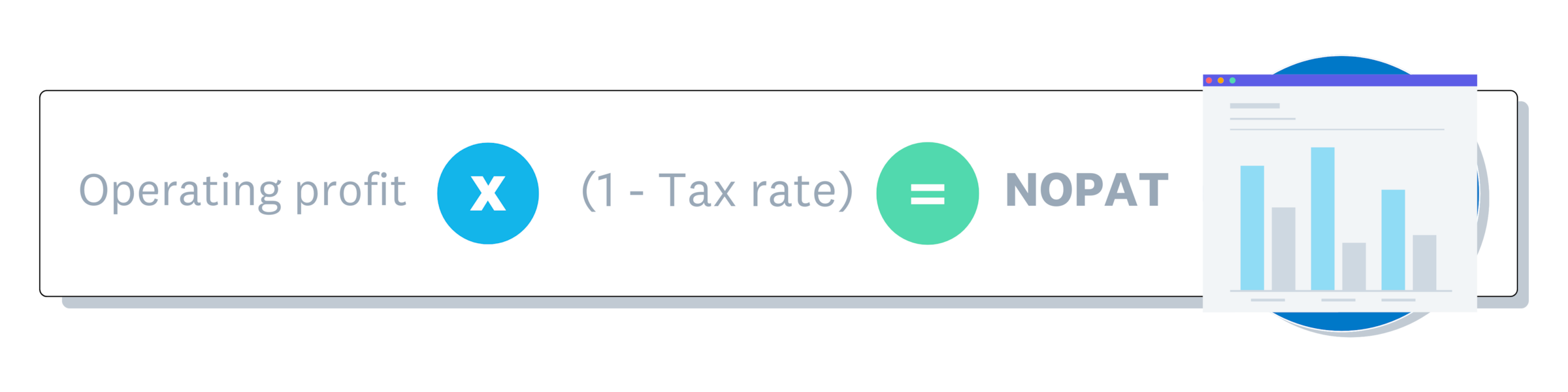

NOPAT formula explained

The NOPAT formula converts operating profit to an after-tax figure:

NOPAT = Operating Profit × (1 − Tax Rate)

Formula components:

- operating profit: revenue minus operating expenses (including depreciation and amortisation), but before taxes and interest

- tax rate: your effective tax rate, calculated as taxes paid divided by operating profit

- (1 − Tax Rate): the portion of profit retained after taxes

Example:

- Operating profit: $100,000

- Tax rate: 20%

- NOPAT: $100,000 × (1 − 0.20) = $80,000

Operating profit differs slightly from EBIT (Earnings Before Interest and Taxes). EBIT includes all income sources, while operating profit only includes income from core business activities.

How to calculate NOPAT

Apply the formula using your operating profit and tax rate to get your NOPAT figure.

Determine operating profit

Operating profit represents your earnings from core business activities before taxes and interest.

Calculate it using this path:

- Start with revenue from your main business activities

- Subtract cost of goods sold to get gross profit

- Subtract operating expenses (rent, salaries, utilities, depreciation) to get operating profit

Formula: Operating Profit = Revenue − Cost of Goods Sold − Operating Expenses

Exclude any non-operating income such as investment gains or rental income from non-core assets.

Find the tax rate

Your effective tax rate determines how much of your operating profit goes to taxes.

Two approaches to find your tax rate:

- historical method: divide last year's income tax by pre-tax income (for example, $20,000 tax ÷ $100,000 income = 20%)

- statutory method: use your jurisdiction's corporate tax rate if you expect consistent taxation

If your business is growing significantly, consider whether you'll move into a higher tax bracket and adjust your rate accordingly.

Apply the formula

Apply the formula using your operating profit and tax rate:

Sample calculation:

- Operating profit: $50,000

- Tax rate: 25%

Steps:

- Calculate the after-tax multiplier: 1 − 0.25 = 0.75

- Multiply: $50,000 × 0.75 = $37,500 NOPAT

Your core business operations generate $37,500 in profit after taxes, regardless of how you've financed the business. Use this figure to compare against competitors, calculate EVA, or assess operational improvements over time.

NOPAT calculation example

Let's walk through a complete NOPAT calculation for a small retail business.

Scenario: Coastal Surf Shop

- Annual revenue: $500,000

- Cost of goods sold: $200,000

- Operating expenses: $150,000

- Interest on business loan: $15,000

- Effective tax rate: 25%

Step 1: Calculate operating profit$500,000 − $200,000 − $150,000 = $150,000 operating profit

Step 2: Apply the NOPAT formula$150,000 × (1 − 0.25) = $150,000 × 0.75 = $112,500 NOPAT

Coastal Surf Shop generates $112,500 in after-tax profit from its core retail operations. This figure excludes the $15,000 in loan interest, so you can evaluate the business's operational strength separately from its financing decisions.

If you were comparing this shop to a competitor with no debt, NOPAT provides an equal basis for comparison.

How businesses use NOPAT

NOPAT serves several purposes in financial analysis and business valuation. Here are the most common applications:

Business valuation and DCF analysisDiscounted cash flow (DCF) models often start with NOPAT to project future operational earnings. Because NOPAT excludes financing effects, it provides a cleaner foundation for valuing a company's operations.

Performance benchmarkingCompare your operational efficiency against competitors without debt structures skewing the results. NOPAT reveals which business generates more profit from similar operations.

Return on invested capital (ROIC)Calculate ROIC by dividing NOPAT by total invested capital. This shows how effectively a business converts capital into operational profits, and while thresholds are firm-specific, the minimum ROIC tends to be between 10% and 15% for many investors.

Merger and acquisition analysisBuyers use NOPAT to assess target companies' true operational performance, separate from existing financing arrangements they may restructure post-acquisition.

Economic Value Added (EVA)As covered earlier, NOPAT is the starting point for EVA calculations that measure value creation beyond the cost of capital.

NOPAT vs net income

NOPAT excludes financing costs and non-operating items, while net income includes everything.

- Operating revenue: included in both NOPAT and net income

- Operating expenses: included in both NOPAT and net income

- Taxes: included in both NOPAT and net income

- Interest expenses: excluded from NOPAT, included in net income

- Non-operating income: excluded from NOPAT, included in net income

Example: A bakery's financials

- Net income: $100,000

- Includes: $12,000 rental income (non-operating)

- Includes: $8,000 interest expense

To calculate NOPAT, remove the non-operating rental income and add back the interest expense:$100,000 − $12,000 + $8,000 = $96,000 NOPAT

If a business has no debt and no non-operating income, NOPAT and net income will be identical.

Operating profit vs NOPAT

Operating profit measures earnings before both taxes and interest, while NOPAT accounts for taxes.

The relationship:NOPAT = Operating profit × (1 − Tax Rate)

Example:

- Operating profit: $96,000

- Tax rate: 16.7%

- NOPAT: $96,000 × (1 − 0.167) = $80,000

Operating profit shows pre-tax operational performance. NOPAT shows what remains after the tax obligation.

NOPAT vs EBITDA

NOPAT and EBITDA both measure operational performance, but they treat taxes and depreciation differently.

Key differences:

- tax treatment: NOPAT reflects actual tax obligations; EBITDA ignores them entirely

- depreciation and amortisation: NOPAT includes these non-cash expenses; EBITDA adds them back

- cash flow indication: EBITDA approximates cash generation; NOPAT measures accounting profit

When to use each:

- use NOPAT when tax impact matters or when comparing businesses across different tax jurisdictions

- use EBITDA when assessing cash generation potential or comparing capital-intensive businesses with varying depreciation policies

NOPAT vs EBIT

NOPAT and EBIT (Earnings Before Interest and Taxes) are closely related but not identical. The key difference is tax treatment. Taxes are excluded from EBIT, but included in NOPAT.

The relationship:NOPAT = EBIT × (1 − Tax Rate)

Example:

- EBIT: $100,000

- Tax rate: 25%

- NOPAT: $100,000 × 0.75 = $75,000

When to use each:

- use EBIT for quick operational comparisons where tax differences aren't relevant

- use NOPAT when you need after-tax figures for valuation, EVA calculations, or comparing businesses in different tax jurisdictions

NOPAT vs free cash flow

NOPAT measures profitability while free cash flow (FCF) measures actual cash generated. They serve different analytical purposes.

Key differences:

- FCF reflects cash reality: it accounts for capital investments and working capital needs that NOPAT ignores

- NOPAT is a starting point: unlevered free cash flow calculations often begin with NOPAT, then adjust for non-cash items and capital requirements

Simplified relationship:Unlevered FCF = NOPAT + Depreciation − Capital Expenditures − Change in Working Capital

When to use each:

- use NOPAT for profitability analysis and operational comparisons

- use FCF for assessing a company's ability to fund growth, pay dividends, or service debt

Track your financial performance with Xero

Understanding NOPAT helps you evaluate business performance, compare investment opportunities, and make informed financial decisions.

Calculating NOPAT is straightforward when your financial data is organised and accessible. Xero helps you track income, expenses, and taxes in one place, so you can generate the reports you need for NOPAT analysis and other financial metrics.

Get one month free and see how Xero makes financial analysis easier for your business.

FAQs on NOPAT

Here are answers to common questions about NOPAT and how it compares to other financial metrics.

Is NOPAT the same as EBIT?

No. NOPAT includes taxes while EBIT excludes them. The formula connecting them is: NOPAT = EBIT × (1 − Tax Rate).

Why use NOPAT in DCF analysis?

NOPAT provides tax-adjusted operational earnings that reflect the true cost of doing business. DCF models use NOPAT as a foundation because it isolates operational performance from financing decisions. This gives a cleaner basis for projecting future cash flows.

When should I use NOPAT vs EBITDA?

Use NOPAT when tax impact matters or when comparing businesses across different tax jurisdictions. Use EBITDA when comparing capital-intensive businesses or when you want to approximate cash generation before depreciation effects.

Can NOPAT be negative?

Yes. NOPAT will be negative if operating profit is negative, meaning the business loses money on its core operations before considering financing costs. A negative NOPAT signals operational problems that need addressing.

How often should I calculate NOPAT?

Calculate NOPAT quarterly or annually to track operational performance trends. More frequent calculations may be useful during detailed valuation work or when monitoring significant operational changes.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.