Solvency vs liquidity: what's the difference for you?

Learn how solvency vs liquidity helps you manage cash, meet bills, and plan sustainable growth.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Tuesday 24 February 2026

Table of contents

Key takeaways

- Monitor both solvency and liquidity regularly since they measure different timeframes—liquidity shows your ability to pay bills in the coming weeks or months, while solvency indicates whether your business can survive and meet long-term debt obligations over years.

- Calculate your current ratio by dividing current assets by current liabilities to assess short-term financial health, aiming for a ratio above 1.0 which indicates you have enough resources to cover immediate obligations.

- Improve liquidity by speeding up customer payments, building cash reserves for unexpected expenses, and monitoring cash flow timing to ensure you can meet short-term commitments without disrupting operations.

- Strengthen solvency by maintaining consistent profitability, managing debt wisely through favourable loan terms, and ensuring your total assets exceed total liabilities to demonstrate long-term financial stability to lenders and investors.

What does liquidity mean in business?

measures your ability to pay bills and make loan repayments in the coming months. It compares your current assets (cash, inventory, and receivables) against current liabilities (amounts owed within your operating cycle, the time between acquiring assets and their final cash realisation), which is typically one year.

Liquidity is commonly expressed as a ratio, such as the current ratio, quick ratio, or cash ratio. A higher ratio means you have more resources available to cover short-term obligations.

Other liquidity ratios

The current ratio is the most common liquidity measure for small businesses, but two other ratios provide additional insight:

- Quick ratio (acid test ratio): Current assets minus inventory and prepaid expenses, divided by current liabilities. This shows whether you can meet obligations without selling inventory.

- Cash ratio: Cash and cash equivalents divided by current liabilities. This is the most conservative measure, showing immediate payment ability.

Learn more in this guide on liquidity ratios.

How liquid are your assets?

Asset liquidity refers to how quickly you can convert an asset to cash. Here's how common business assets rank:

- Cash: Your most liquid asset. Physical currency and bank funds can be accessed immediately.

- Accounts receivable: Invoices owed to you convert to cash relatively quickly. Shorter payment terms mean higher liquidity.

- Inventory: Can be sold for cash, but timing varies based on demand and market conditions. For some businesses, the operating cycle is longer than one year; a distillery, for example, may classify its inventory as a current asset for over two decades.

- Physical assets: Buildings, equipment, and vehicles are the least liquid. Selling these can take months.

Liquidity vs other financial concepts

Liquidity is often confused with related financial concepts. Here's how they differ:

- Liquidity: Shows whether you can cover upcoming costs with available assets.

- Cash flow: Tracks the movement of cash in and out of your business over time.

- Working capital: The amount remaining after subtracting current liabilities from current assets.

- Free cash flow: Cash left after making capital investments, available for growth or debt repayment.

How does liquidity affect business growth?

Strong liquidity supports business growth by helping you:

- Seize opportunities: Launch new products, hire staff, or invest in equipment without waiting for financing.

- Handle unexpected costs: Cover emergency repairs, equipment failures, or sudden expenses without disrupting operations.

- Maintain stability: Negotiate from strength with suppliers and lenders instead of scrambling for alternatives.

What does solvency mean in business?

Solvency refers to your ability to meet long-term financial commitments. A solvent business has positive net equity, meaning total assets exceed total liabilities.

In practical terms, solvency shows whether your business can survive and pay its debts over years, not just months. If liabilities exceed assets, your business is technically insolvent.

What factors affect your solvency?

Three factors affect your solvency:

- Profitability: Consistent profits keep your balance sheet healthy and assets exceeding liabilities.

- Debt management: Negotiate favourable loan terms and understand the consequences of missed payments on secured debt.

- Asset utilisation: Generate returns from your assets that exceed your debt obligations, and minimise waste through tracking.

What is solvency vs profitability?

Solvency and profitability are related but distinct:

- Profitability: Whether your revenue exceeds your costs

- Solvency: Whether your total assets exceed your total liabilities

A profitable business is more likely to stay solvent because profits build assets over time. However, profitability alone doesn't guarantee solvency. Taking on excessive debt can push liabilities above assets, leading to insolvency even if the business is profitable.

Learn more about profitability.

How does solvency affect your business growth?

Strong solvency helps you:

- Access financing: Banks and lenders offer better terms when they're confident you can repay.

- Attract investors: Potential investors see a stable foundation for growth.

- Negotiate with suppliers: Cash reserves let you buy in bulk and reduce per-unit costs.

- Plan for the future: Financial stability supports long-term business decisions.

The main differences between solvency and liquidity

Solvency takes a long-term view of your financial health, while liquidity focuses on the short term. The key differences are:

- Timeframe: Liquidity covers weeks to months; solvency covers years.

- Focus: Liquidity measures cash availability; solvency measures overall asset-to-debt balance.

- Risk addressed: Poor liquidity means you can't pay bills; poor solvency means you can't survive long-term.

The table below outlines these and other differences.

Table of the difference between solvency and liquidity

Monitor both metrics regularly to maintain a complete picture of your financial health.

How to measure solvency and liquidity in your business

Use these formulas to calculate your solvency and liquidity ratios. Both metrics help you assess different aspects of your financial health.

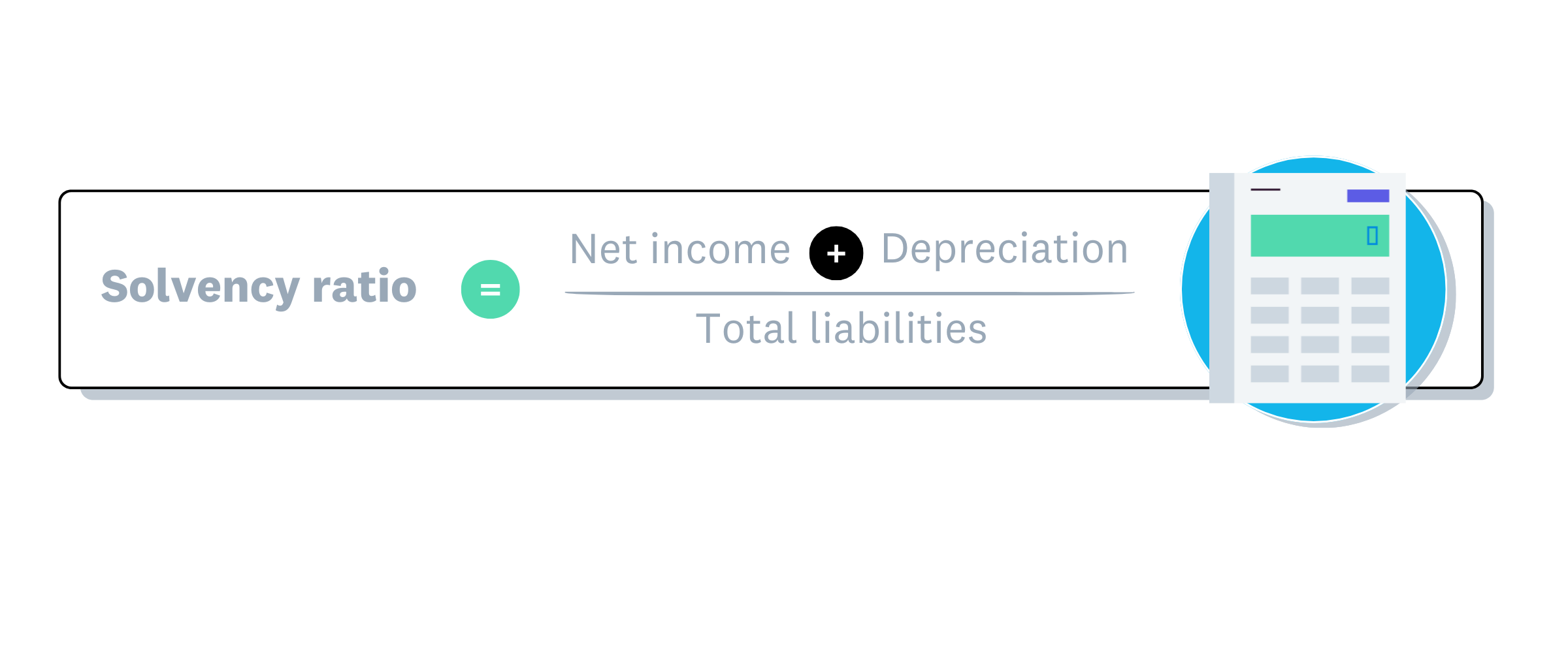

Solvency ratio formula

Solvency ratio formula

Depreciation is the decrease in asset value over time due to wear and tear, recorded as a deduction on your balance sheet.

Solvency ratio example

Martha owns a cafe with:

- Net income: $50,000

- Depreciation: $10,000

- Total liabilities: $300,000

Calculation: ($50,000 + $10,000) ÷ $300,000 = 20%

A solvency ratio of 20% or above is generally considered healthy. Martha's cafe has a good chance of meeting its long-term debt obligations.

You can also calculate liquidity ratios to assess your short-term financial health.

Liquidity ratio formula

There are several liquidity ratios, like the cash ratio, quick ratio, and the working capital ratio, which is a useful long-term measure of liquidity.

Here's the formula for the working capital ratio:

Liquidity ratio example (current ratio)

Sadiq runs a sports shop with:

- Current assets: $120,000

- Current liabilities: $80,000

Calculation: $120,000 ÷ $80,000 = 1.5

A current ratio above 1.0 indicates good liquidity. Sadiq's ratio of 1.5 means he has $1.50 in current assets for every $1.00 of short-term debt, so he can likely meet his upcoming financial commitments.

Why solvency and liquidity matter for your small business

Why solvency matters

A solvent business is financially stable. It can absorb risks like unpaid invoices, invest in growth, and maintain shareholder confidence, all critical functions for the small and medium-sized businesses that contribute up to 55% of Gross Domestic Product (GDP) in developed economies. Poor solvency leads to trouble paying debts, and insolvency can result in bankruptcy.

Why liquidity matters

A liquid business has enough cash to pay suppliers and staff on time. Strong liquidity also provides a buffer against unexpected costs, slow periods, or market changes.

Why track both

Monitoring solvency and liquidity together helps you make better decisions for daily operations and long-term planning. One metric alone doesn't tell the full story.

Tips to improve your financial solvency and liquidity

Here are practical ways to strengthen both your solvency and liquidity.

To improve solvency:

- Attract investors: Bring in new capital to boost your asset base.

- Restructure debt: Renegotiate, refinance, or consolidate loans for better terms.

- Reduce costs: Review expenses and adjust operations to improve profitability.

To improve liquidity:

- Monitor cash flow: Track inflows and outflows, and time payments accordingly.

- Benchmark performance: Compare your ratios against industry standards, often with an accountant's help. A global survey found that 86% of small and medium accounting practices provide some form of advisory/consulting service to help businesses with financial planning and performance.

- Speed up collections: Make it easier for customers to pay invoices promptly.

- Build reserves: Maintain a cash buffer for unexpected expenses.

With the right tools, tracking these metrics becomes much easier.

Use Xero to track your solvency and liquidity

Xero accounting software gives you real-time visibility into your financial health. Track daily cash flow for liquidity insights, or run financial reports to monitor long-term solvency.

See how Xero can help you stay on top of your numbers. Get one month free.

FAQs on solvency and liquidity

Here are answers to some common questions about solvency and liquidity.

What does it mean to provide liquidity?

Providing liquidity means ensuring your business has enough cash to cover short-term obligations. You can improve liquidity by speeding up customer payments, reducing expenses, or securing a line of credit.

Can my business have good solvency but poor liquidity?

Yes, this is common. A business can be solvent (assets exceed liabilities) but have poor liquidity if most assets are tied up in property, equipment, or inventory. For example, a business with valuable land but little cash may struggle to pay next month's bills while still being financially stable long-term.

Is solvency good or bad?

Solvency is positive. It means your business can meet its long-term financial obligations because your assets exceed your liabilities. A solvent business is financially stable and better positioned to access credit, attract investors, and weather economic downturns.

Is high solvency good?

Yes, higher solvency generally indicates stronger financial health. It means you have more assets relative to liabilities, which reduces risk for lenders and investors. However, extremely high solvency could suggest you're not using available capital for growth opportunities.

What is a good solvency ratio for my small business?

A solvency ratio of 20% or higher is generally considered healthy, though benchmarks vary by industry. Capital-intensive industries like manufacturing may have lower typical ratios than service businesses. Compare your ratio against industry peers for the most relevant assessment.

What's the difference between liquidity and working capital?

Liquidity measures your ability to pay short-term obligations, expressed as a ratio. Working capital is the actual dollar amount remaining after subtracting current liabilities from current assets. Both assess short-term financial health, but liquidity ratios make it easier to compare businesses of different sizes.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.