Accounting software for your Irish small business

Want to get more productive? Xero’s easy-to-use bookkeeping software helps you rattle through jobs – whether it’s automating your invoicing, managing your cash flow, or running customised reports for crucial financial insights. You do more in less time, and get back to running your business.

Join over 4.2 million subscribers using Xero

Awards and recognition for our work

Streamline your invoicing

Get your invoices out faster with Xero’s templates. Then track payments and send automatic reminders.

Accept online payments and get paid sooner

Add a Pay now button to your invoices and give your customers multiple ways to pay you with less hassle.

Track your inventory levels precisely

Always know what you have in stock with real-time data. Automate your purchase orders for a slick process.

Connect your business bank accounts

Want to master your cash flow? Get all your bank transactions on a single screen in Xero.

Smooth out your payday kinks

Xero’s automatic pay runs streamline the process – and make sure everyone is paid on time, every time.

Control your project costs

Xero’s tools help you accurately track your time and project costs – all in one clever piece of software.

Xero can power up your small business in big ways. All features of Xero accounts software

Plans to suit your business

All pricing plans cover the accounting essentials, with room to grow.

Save yourself hours with Xero accounting software

Short on time? Xero’s smart tools automate admin, track finances, and provide insights—helping you stay organized and grow your business.

Paperless record-keeping

Keep all your financial records in one central place with Xero online accounting software. Never lose a receipt!

Automations that fast-track your admin

Save time on your jobs, from automating your invoice reminders to managing your business expenses.

Smart data and insights to grow your business

Make confident decisions with sophisticated trend analysis and clear, comprehensive reports tailored to your business.

Get your bank feed in Xero

No more hopping from screen to screen! Just log in to your Xero organisation to check your bank feed and reconcile transactions with Xero’s automations. That way you can update your figures fast, know when to pay your suppliers, and better manage your cash flow.

- Xero connects to the Bank of Ireland and Allied Irish Bank

- Xero pulls your bank transactions into your Xero organisation each business day

- The Xero Accounting app lets you reconcile your transactions away from your desk – even while travelling

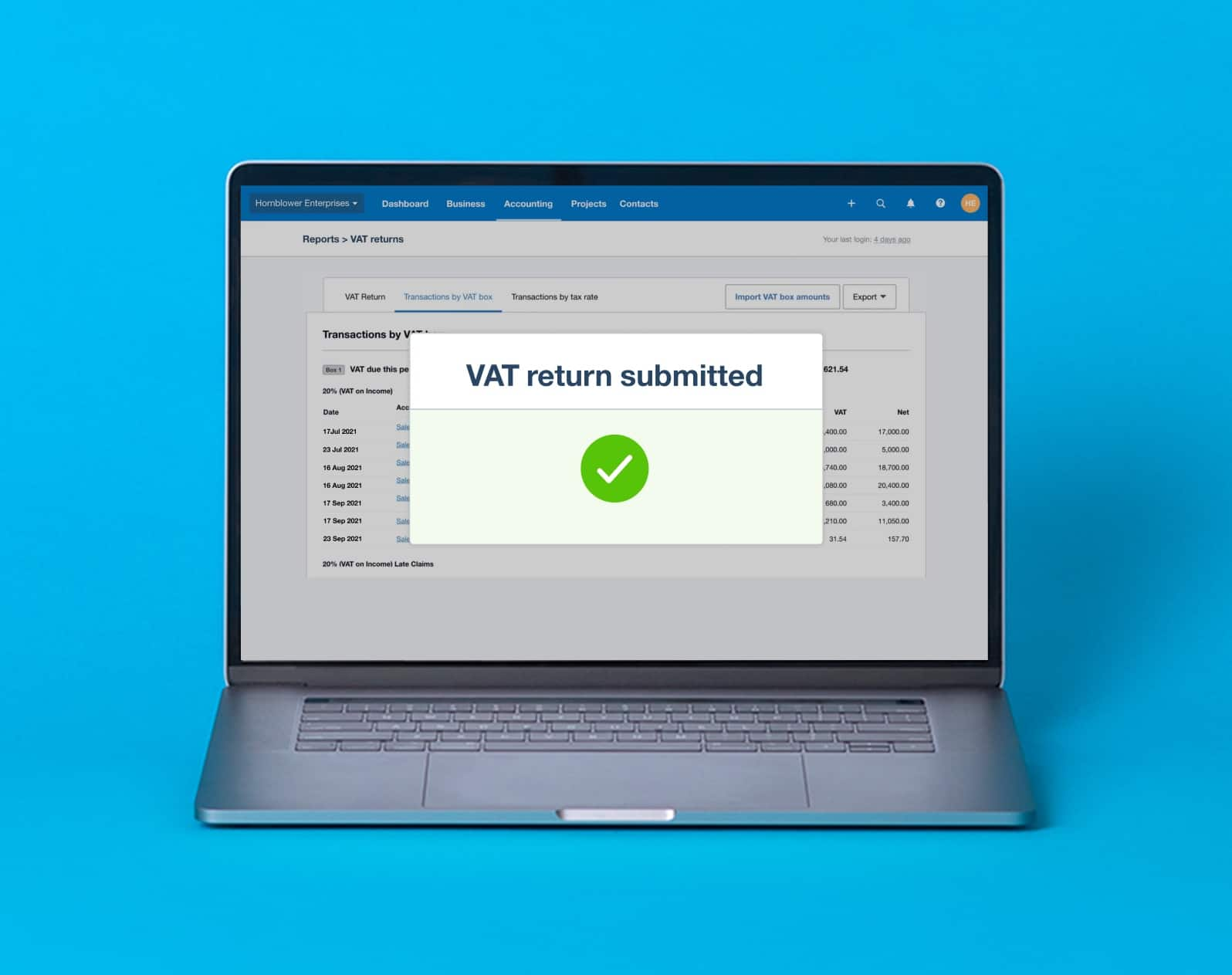

Your VAT compliance in the bag

Xero is a powerful bookkeeping software for your small business taxes. Want faultless numbers? Automatic calculations help prevent mistakes in your VAT (value added tax) returns. How about faster reports? Xero gathers the right info for your tax period and helps with your tax filings.

- Set up as many tax rates as you need for your business

- Automatically calculate VAT on your invoices, quotes, and purchase orders

- Run sales tax reports to quickly pull together the right figures for your VAT forms

Apps to boost your business

Xero integrates beautifully with hundreds of third-party apps so you can do more for your business, from improving your inventory management to transforming the way you communicate with shareholders. Explore the Xero App Store for inspiration across a range of popular categories.

- Apps for bills and expenses, reporting, professional services, CRM, invoicing, and much more

- Apps to support your financial and HR compliance, like Parolla and SimplePay

- Data flows between your Xero organisation and your apps, keeping all your figures up to date

Your best fit: Xero versus other accounting software

Find out how Xero compares with other accounting software in Ireland.

| Xero | Quickbooks | MYOB | HNRY | |

|---|---|---|---|---|

| Sign up with no credit card | ||||

| Cancel anytime | ||||

| Bank reconciliation | ||||

| Inventory |

Getting Xero made the whole business more efficient. It made accessing the accounts so much easier.

Xero lets Sidonie from Papersmiths focus on other parts of her business

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.

FAQs on accounting software

Xero’s cloud-based software lets you handle your financial admin wherever you have an internet connection. Irish small business owners can zip through their jobs on the go – reconcile your bank transactions, make online payments, reimburse expenses, and lots more. You don’t need to download any software; all you need is a multi-factor authentication (MFA) app to log in to your Xero organisation. Xero then regularly backs up your data and protects it with multiple layers of security.

See why Xero cloud accounting software is good for your businessXero’s cloud-based software lets you handle your financial admin wherever you have an internet connection. Irish small business owners can zip through their jobs on the go – reconcile your bank transactions, make online payments, reimburse expenses, and lots more. You don’t need to download any software; all you need is a multi-factor authentication (MFA) app to log in to your Xero organisation. Xero then regularly backs up your data and protects it with multiple layers of security.

See why Xero cloud accounting software is good for your businessNo, but it’s very useful. The mobile app works with Xero accounting software to help you run your small business from anywhere. Keep track of your unpaid and overdue invoices, bank account balances, profit and loss, cash flow, and bills to pay. You can also reconcile bank accounts and convert quotes to invoices. The mobile app is free with every subscription, and is compatible with iOS and Android.

See how to stay connected to your business on the goNo, but it’s very useful. The mobile app works with Xero accounting software to help you run your small business from anywhere. Keep track of your unpaid and overdue invoices, bank account balances, profit and loss, cash flow, and bills to pay. You can also reconcile bank accounts and convert quotes to invoices. The mobile app is free with every subscription, and is compatible with iOS and Android.

See how to stay connected to your business on the goYes, but an accountant’s expertise can help your business perform. But if you choose not to engage one, read online resources – like those by Xero – to help you manage cash flow, track payments, and create invoices. They also keep you up with regulatory changes around tax and record keeping, for example. And don’t forget cloud accounting software like Xero – it keeps all your financial records in one secure place, and its automated calculations prevent mistakes, save you time, and make tax season easier.

Here’s how to convert to Xero from other accounting softwareYes, but an accountant’s expertise can help your business perform. But if you choose not to engage one, read online resources – like those by Xero – to help you manage cash flow, track payments, and create invoices. They also keep you up with regulatory changes around tax and record keeping, for example. And don’t forget cloud accounting software like Xero – it keeps all your financial records in one secure place, and its automated calculations prevent mistakes, save you time, and make tax season easier.

Here’s how to convert to Xero from other accounting softwareThere are three basic steps to setting up an accounting system. The aim is to keep everything simple and accurate. First, open a dedicated business account for all your incoming and outgoing payments. Second, decide which accounting method (cash or accrual) suits your business. Third, choose accounting software, such as Xero, that has the features you need, like the ability to use eInvoicing and send foreign currency payments.

There are three basic steps to setting up an accounting system. The aim is to keep everything simple and accurate. First, open a dedicated business account for all your incoming and outgoing payments. Second, decide which accounting method (cash or accrual) suits your business. Third, choose accounting software, such as Xero, that has the features you need, like the ability to use eInvoicing and send foreign currency payments.

It’s easy to use Xero’s basic features. The software is intuitive, so people with no accounting or finance background can learn the basics quickly. It’s easy to connect your bank so your transactions flow into Xero, and to create professional invoices from scratch. Xero has all sorts of resources on business and finance topics to help, all written in plain English for when you want clear, simple answers. If you’re still unsure, Xero users can contact our support team 24/7 for help.

It’s easy to use Xero’s basic features. The software is intuitive, so people with no accounting or finance background can learn the basics quickly. It’s easy to connect your bank so your transactions flow into Xero, and to create professional invoices from scratch. Xero has all sorts of resources on business and finance topics to help, all written in plain English for when you want clear, simple answers. If you’re still unsure, Xero users can contact our support team 24/7 for help.

Yes, you aren’t required to have an accountant in most regions so you can certainly run your business without one. However, it can be beneficial to bring one on and utilise their expertise to help your business perform. Online resources – such as those by Xero – explain topics like managing cash flow, tracking payments, and creating invoices. Read these materials to stay up to date with regulatory and other changes around tax and record keeping. Cloud-based accounting software like Xero is a big help. This keeps all your financial records in one secure place. Its automated calculations prevent data entry mistakes, save you time, and make tax season easier. And you can always get expert advice from an accountant.

Check out Xero’s directory of accountants and bookkeepersYes, you aren’t required to have an accountant in most regions so you can certainly run your business without one. However, it can be beneficial to bring one on and utilise their expertise to help your business perform. Online resources – such as those by Xero – explain topics like managing cash flow, tracking payments, and creating invoices. Read these materials to stay up to date with regulatory and other changes around tax and record keeping. Cloud-based accounting software like Xero is a big help. This keeps all your financial records in one secure place. Its automated calculations prevent data entry mistakes, save you time, and make tax season easier. And you can always get expert advice from an accountant.

Check out Xero’s directory of accountants and bookkeepersTechnically, yes. But it can be a time-consuming process to work across different data sources and tools. Accounting software like Xero does this work for you. Xero keeps all information in one secure place, and makes automatic calculations to keep your records accurate and up to date. Because Xero is based in the cloud, you can log in at any time, from anywhere, and give your accountant and bookkeeper access so you can easily work with them on your finances.

Technically, yes. But it can be a time-consuming process to work across different data sources and tools. Accounting software like Xero does this work for you. Xero keeps all information in one secure place, and makes automatic calculations to keep your records accurate and up to date. Because Xero is based in the cloud, you can log in at any time, from anywhere, and give your accountant and bookkeeper access so you can easily work with them on your finances.

See more of what Xero can do

What to explore next in Xero

Xero’s online accounting software is designed to make life easier for small businesses – anywhere, any time.