Accumulated depreciation: definition and calculation

Learn if accumulated depreciation is an asset, how it affects your balance sheet, and how to calculate it.

Written by Jotika Teli—Certified Public Accountant with 24 years of experience. Read Jotika's full bio

Published Monday 23 February 2026

Table of contents

Key takeaways

- Calculate your asset's current book value by subtracting accumulated depreciation from the original cost to understand what your assets are actually worth today.

- Use the straight-line depreciation method to spread costs evenly across an asset's useful life by dividing the asset cost minus salvage value by its useful life in years.

- Record accumulated depreciation as a contra asset account with a credit balance on your balance sheet to offset the original asset value and show realistic worth.

- Track accumulated depreciation to reduce your taxable income through depreciation expenses while planning for future asset replacements and maintenance costs.

What is accumulated depreciation?

Accumulated depreciation is the total depreciation recorded for an asset since you bought it. It shows how much value the asset has lost over time due to wear and tear. Official financial statements show a company's total accumulated depreciation and impairment. For example, one company reported 2,950 thousand currency units for its property, plant, and equipment.

Tracking accumulated depreciation lets you calculate the asset's book value: what it's realistically worth today. The formula is simple: asset cost minus accumulated depreciation equals book value.

Here are two examples:

- Office furniture: Cost $5,000 with $1,000 annual depreciation. After three years, accumulated depreciation totals $3,000, leaving a book value of $2,000.

- Machinery: Cost $25,000 with $2,500 annual depreciation. After six years, accumulated depreciation totals $15,000, leaving a book value of $10,000.

Depreciation vs accumulated depreciation

Depreciation is a periodic expense that records an asset's value decrease over a set time. A company's depreciation charge for the year can be significant. For example, one IFRS example shows 950 thousand currency units.

Accumulated depreciation is the running total of all depreciation expenses recorded for that asset. Each time you record depreciation, accumulated depreciation increases.

The key difference: depreciation is a single period's expense, while accumulated depreciation is the sum of all periods combined.

How accumulated depreciation works

Accumulated depreciation builds up over time as you record depreciation expenses each accounting period. It's a running total that grows with every depreciation entry.

Here's the process:

- You purchase an asset and record its original cost.

- Each period (monthly, quarterly, or yearly), you record a depreciation expense.

- That expense adds to the accumulated depreciation account. For example, one company's financial statement showed its accumulated depreciation... increased from 1,200 to 1,500 thousand currency units for its buildings in a single year.

- The asset's book value decreases by the same amount.

For example, if you depreciate equipment by $500 each month:

- After month one, accumulated depreciation is $500.

- After month two, it's $1,000.

- After month three, it's $1,500.

The accumulated depreciation account is tracked separately from the asset itself. This lets you see both the original cost and how much value has been used up.

Is accumulated depreciation an asset or a liability?

Accumulated depreciation is neither an asset nor a liability. It's a contra asset account.

A contra asset offsets the original value of assets on your balance sheet. Unlike liabilities, accumulated depreciation doesn't represent money you owe. It simply reduces an asset's recorded value over time.

Here's how it works:

- You record accumulated depreciation alongside your other assets.

- It carries a credit (negative) balance.

- This negative balance reduces the asset's original cost to show its current book value. In one IFRS for SMEs example, book value is calculated as the original cost less CU300,000 accumulated depreciation.

The result is a more realistic picture of what your assets are actually worth.

How to calculate accumulated depreciation

Here's how to calculate accumulated depreciation step by step. The examples below use the straight-line method: a common approach for small businesses, featured in IFRS for SMEs guidance, because it spreads depreciation evenly across an asset's useful life. For example, a firm with a machine that it estimates has a 10-year useful life would depreciate it evenly over that decade.

The straight-line depreciation calculation

Calculate annual depreciation expense with this formula:

Annual depreciation expense = (cost of asset − salvage value) ÷ useful life

Here's what each term means:

- Cost of asset: The original purchase price

- Salvage value: The estimated resale or scrap value when the asset is no longer usable

- Useful life: The number of years the asset will remain functional

Calculate straight-line depreciation

Here's a worked example using an asset that costs $1,000, has a five-year useful life, and a $100 salvage value.

Step 1: Calculate annual depreciation expense

Apply the formula:

($1,000 − $100) ÷ 5 = $180 per year

Step 2: Track accumulated depreciation each year

Create a depreciation schedule showing how accumulated depreciation grows:

- Year one: $180

- Year two: $360

- Year three: $540

- Year four: $720

- Year five: $900

Step 3: Calculate book value at any point

Use this formula: Book value = original cost − accumulated depreciation

After three years, the book value is: $1,000 − $540 = $460

Other depreciation methods

Straight-line isn't the only way to calculate depreciation. Two other common methods are:

- Declining balance method: Applies a fixed percentage to the asset's remaining book value each year, resulting in higher depreciation early on

- Double-declining balance method: Similar to declining balance but uses double the straight-line rate for even faster early depreciation

Most small businesses use straight-line because it's simple and spreads costs evenly. However, accelerated methods like declining balance can be useful for assets that lose value quickly in their first few years.

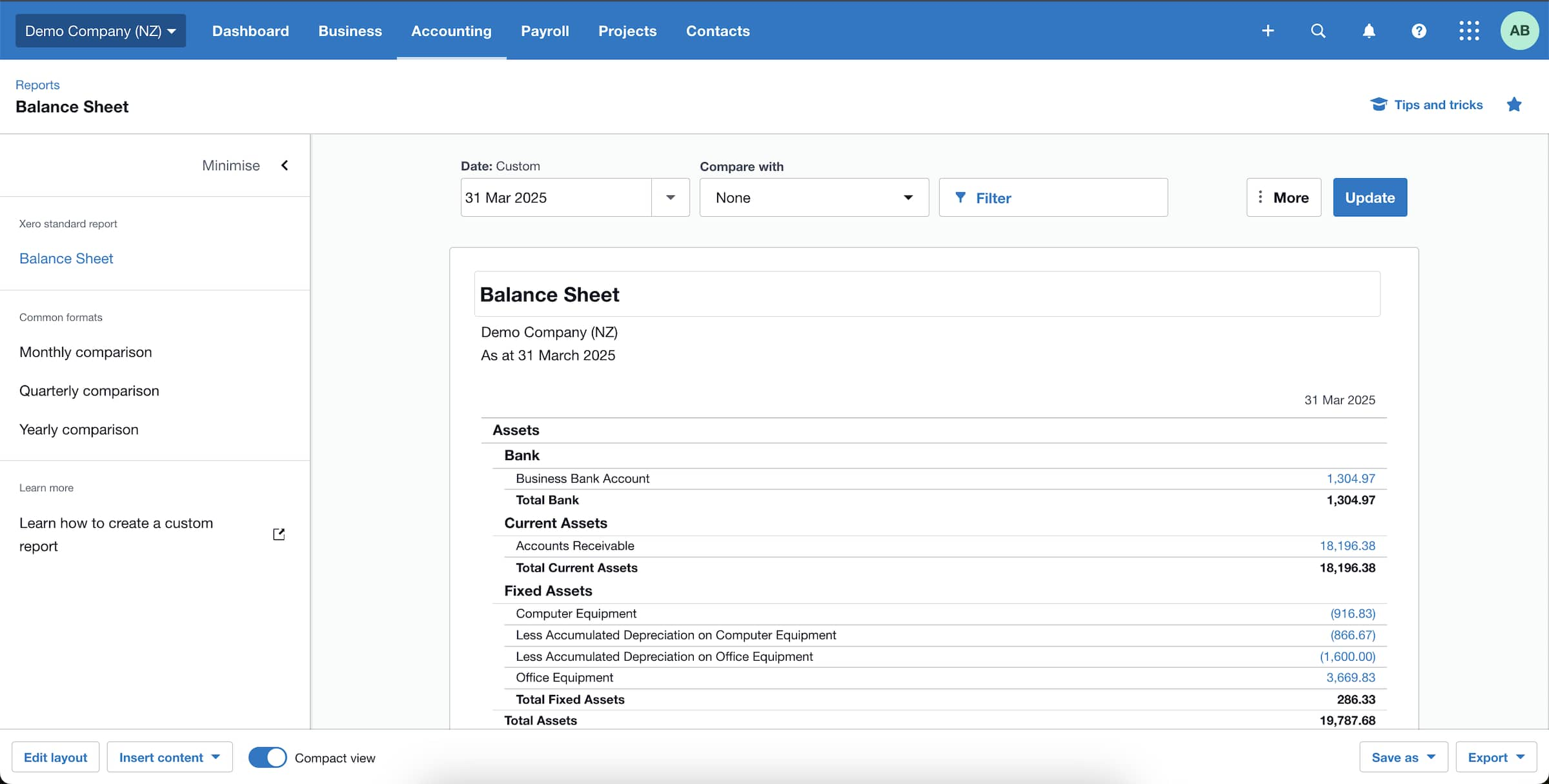

Example: Balance sheet for accumulated depreciation

The balance sheet below shows how accumulated depreciation appears in practice. Notice how it's listed directly under the asset's original cost, reducing the total to show net book value.

How does accumulated depreciation affect financial statements?

Accumulated depreciation affects three key financial statements differently.

Accumulated depreciation on the balance sheet

Accumulated depreciation reduces an asset's book value. Your balance sheet shows the original cost, then subtracts accumulated depreciation to display the asset's current worth.

Accumulated depreciation on the income statement

Depreciation expense reduces your taxable income each period. As a non-cash expense, it lowers reported profits without any money leaving your business.

Accumulated depreciation on the cash flow statement

Depreciation is added back to net income on the cash flow statement. This adjustment accounts for the fact that depreciation reduces profit on paper but doesn't involve actual cash outflow.

Why understanding accumulated depreciation matters for a business

- Better business planning: Track how asset values change over time to plan replacements, upgrades, and maintenance costs

- Potential tax savings: Depreciation reduces taxable income, lowering your tax bill and keeping more cash in the business

- Easier financing: Accurate book values improve your chances of securing loans or attracting investors

Simplify your accounting with Xero

Tracking accumulated depreciation gets complicated as your business grows, especially when you're managing multiple assets with different useful lives.

Xero simplifies the process by helping you create detailed depreciation schedules and track asset values automatically. You get accurate financial reports without the manual calculations.

Ready to simplify your depreciation tracking? Get one month free and see how Xero can help.

FAQs on accumulated depreciation

Here are answers to common questions about accumulated depreciation.

How does accumulated depreciation affect cash flow?

Accumulated depreciation doesn't directly affect cash flow because it's a non-cash expense: no money leaves your business when you record it. However, it does reduce taxable income, which lowers your tax bill and keeps more cash in the business.

What happens to an asset's accumulated depreciation when you sell it?

When you sell an asset, its accumulated depreciation is removed from your balance sheet along with the asset itself. IFRS guidance shows an example where an entity sold an owner-occupied building. The gain or loss is determined by comparing the sale price to the asset's carrying amount (book value) at that time.

Do I record accumulated depreciation as a debit or a credit?

Record accumulated depreciation as a credit. As a contra asset account, it carries a credit balance that offsets the asset's debit balance, reducing the asset's book value on your balance sheet.

Is accumulated depreciation a current liability?

No, accumulated depreciation is not a current liability. Current liabilities are debts due within 12 months, while accumulated depreciation is a contra asset that reduces an asset's book value; it's not money you owe.

Here's more about current and non-current liabilities.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.