Cash flow forecast: how to create one for your business

Learn how a cash flow forecast helps you spot gaps, plan your spend, and stay funded.

Written by Lena Hanna—Trusted CPA Guidance on Accounting and Tax. Read Lena's full bio

Published Monday 30 March 2026

Table of contents

Key takeaways

- Create both short-term forecasts (covering days to three months for immediate cash needs) and long-term forecasts (covering six months to a year for strategic planning) to get complete visibility over your business finances.

- Update your cash flow forecast at least monthly using a rolling approach where you drop the completed month, add a new month at the end, and adjust figures based on what you've learned from actual results.

- Base your revenue estimates on historical data rather than optimistic projections, and include all irregular expenses like annual subscriptions and quarterly tax payments to avoid cash shortfalls.

- Use the direct forecasting method to track actual cash receipts and payments rather than adjusting profit and loss statements, as this approach is more accurate for small businesses and easier to verify.

What is a cash flow forecast?

A cash flow forecast predicts how much money will flow into and out of your business over a set period. It shows your expected cash position at any point in the future, helping you plan spending and spot potential shortfalls before they happen.

A cash flow forecast differs from a cash flow statement. A statement reports past cash movements, while a forecast projects future ones.

Why is cash flow forecasting important?

Cash flow forecasting helps you avoid cash shortages, pay bills on time, and make confident decisions about spending and growth. When you can see what's coming, you can act before problems arise rather than reacting to them.

For small businesses facing rising costs or unpredictable revenue, forecasting provides the visibility needed to stay in control.

Benefits of cash flow forecasting

Cash flow forecasting offers several benefits for your business:

- Spot cash shortages early: Identify potential gaps before they happen, giving you time to delay spending, request supplier credit, or arrange financing.

- Assess growth affordability: See whether you can afford to buy new equipment, hire staff, or invest in expansion.

- Protect your own pay: Confirm you'll have enough cash to pay yourself as the business owner.

- Track expense trends: Catch rising costs or falling income quickly so you can adjust.

- Fix recurring problems: Identify issues like slow-paying customers, impractical payment terms, or seasonal dips that drain your cash.

What are the key components of a cash flow forecast?

A cash flow forecast includes five key components:

- Opening balance: The cash you have at the start of the forecast period.

- Cash inflows: Money coming in, primarily from sales but also from loans, grants, or asset sales.

- Cash outflows: Money going out for expenses, bills, wages, and other payments.

- Net cash flow: The difference between inflows and outflows, showing whether your cash grew or shrank.

- Closing balance: The cash you expect to have at the end of the period, which becomes your opening balance for the next.

Types of cash flow forecasts

Cash flow forecasts come in different forms depending on how far ahead you're planning and how detailed you need to be. Choosing the right type helps you get useful insights without overcomplicating the process.

Short-term vs long-term forecasts

Short-term forecasts cover days, weeks, or up to three months. They focus on immediate cash needs like paying bills, covering payroll, and managing day-to-day operations. Use short-term forecasts when you need precise timing of cash movements.

Long-term forecasts cover six months to a year or more. They help with strategic planning, such as deciding whether to invest in equipment, hire staff, or expand. This aligns with findings that free cash flow is the most used non-generally accepted accounting principles (GAAP) financial measure for investment analysts making strategic decisions. Long-term forecasts are less precise but give you a broader view of your financial direction.

Most small businesses benefit from maintaining both: a short-term forecast for operational decisions and a longer-term view for planning.

Direct vs indirect forecasting methods

Direct forecasting tracks actual cash receipts and payments. You list specific transactions like customer payments, supplier invoices, and payroll. This method is more accurate for short-term forecasts and easier for small businesses to manage.

Indirect forecasting starts with your profit and loss statement and adjusts for non-cash items like depreciation. It's more common in larger businesses and useful for longer-term projections, a trend supported by research where over 81% of respondents expressed a preference for the indirect method over the direct method.

For most small businesses, the direct method works best because it reflects real cash movements you can track and verify.

How to create a cash flow forecast

Creating a cash flow forecast involves estimating when money will come in and go out, then tracking how those movements affect your cash position over time. The process helps you see exactly when you might face shortfalls or have surplus cash available.

You can build a forecast using a spreadsheet or accounting software. Here's how to do it step by step.

- Start with your current cash position: Note how much cash you have in the bank at the beginning of your forecast period.

- Forecast your income and sales: List all expected cash receipts, including customer payments, grants, tax refunds, and any financing you expect to receive. Include the dates you expect each payment to arrive.

- Estimate your cash inflows: Add up all the money you expect to come in during the period, organised by week or month.

- Estimate your cash outflows: List all expected payments, including regular costs like rent, wages, and supplies. Don't forget irregular expenses like annual subscriptions, quarterly taxes, or planned repairs.

- Compile your forecast: Take your opening balance and work through the period, adding inflows and subtracting outflows. This shows your expected cash position at any point in time.

- Review and compare to actuals: Once the period passes, compare your forecast to what actually happened. This helps you improve accuracy over time.

Creating a cash flow forecast with software

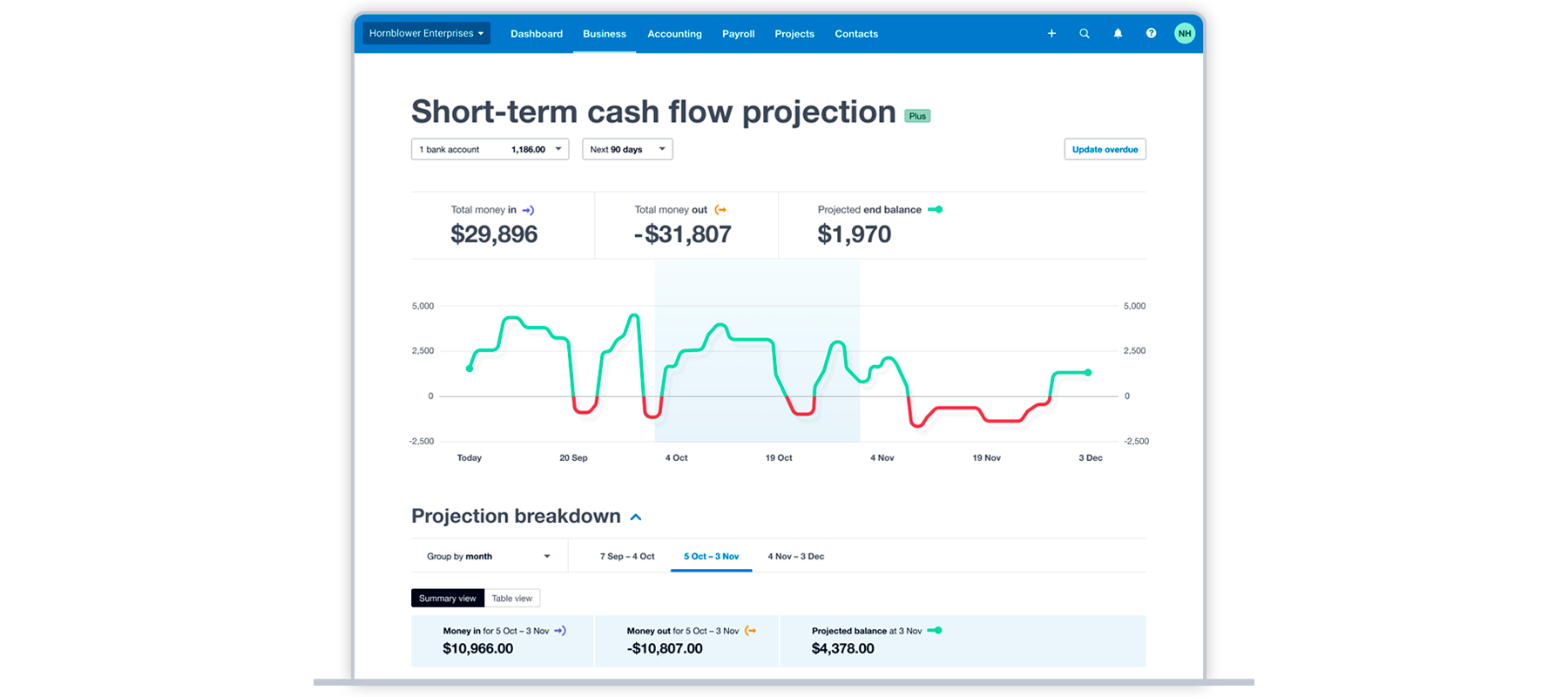

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

A cash flow dashboard shows how cash balances will rise and fall in response to expected transactions.

Accounting software simplifies cash flow forecasting by pulling data directly from your financial records. Research has shown that financial technology has a positive and significant effect on the financial management of micro, small and medium-sized enterprises (MSMEs), allowing you to get forecasts based on real transactions instead of manual figures.

Xero, for example, tracks your income and expenses automatically, which means you can generate a forecast with a few clicks. Key benefits include:

Cash flow forecast example

Here's how a small business might use a cash flow forecast to make an investment decision.

The finance manager of Tiny Construction wants to assess whether the business can afford a new piece of equipment costing $20,000 in the next month.

Based on current bank balances, Tiny Construction has a starting balance of $45,000. Outstanding invoices and sales forecasts estimate incoming payments of $90,000 within the next 30 days. There are no other incoming payments expected for the month.

So the "money in" part of the cash flow projection will look like this:

The "money out" part of the cash flow projection will look like this:

With incoming sales receipts of $90,000 and outgoings of $65,000, the company would have added $25,000 in net cash flow for the period. Adding that to the $45,000 of existing cash will mean the business has $70,000 left in its bank account at the end of the month. This would become their starting balance the following month.

However, if they purchase the equipment with surplus cash, their starting balance for the next month would reduce to $50,000. This example shows how businesses can use cash flow forecasts to make investment decisions and estimate whether they would be able to afford it or would have to consider financing it.

How to analyse your cash flow forecast

Analysing your forecast helps you make better decisions and improve future projections. Focus on these three areas:

- Closing balance: Check the cash you expect to have at the end of each period. If it drops too low, you may need to adjust spending or arrange financing.

- Net cash flow: Look at whether your cash grew or shrank during the period. Consistent negative cash flow signals a problem, even if your closing balance looks healthy.

- Accuracy: Compare your forecast to actual results once the period ends. Identify what you overestimated or underestimated, and adjust your assumptions for next time.

Common cash flow forecasting challenges

Cash flow forecasting isn't always straightforward. Understanding common pitfalls helps you create more accurate forecasts and avoid surprises.

Inaccurate revenue predictions

Overestimating sales is one of the most common forecasting mistakes. Optimistic projections can leave you short when payments don't arrive as expected.

How to avoid it: Base revenue estimates on historical data rather than best-case scenarios. If you're a new business, start conservative and adjust as you gather real data.

Overlooking irregular expenses

Annual subscriptions, quarterly tax payments, and unexpected repairs can create cash gaps if you forget to include them.

How to avoid it: Review the past 12 months of expenses to identify non-monthly costs. Add them to your forecast in the months they're due, not spread evenly across the year.

Not updating regularly enough

A forecast loses value if it doesn't reflect current reality. Outdated projections can lead to poor decisions.

How to avoid it: Set a regular schedule to review and update your forecast, whether that's weekly, fortnightly, or monthly. Use accounting software to reduce the manual effort involved.

How often should you update your cash flow forecast?

Update your cash flow forecast at least monthly, or more often if your business has variable income or tight margins. Regular updates keep your projections accurate and help you catch changes before they become problems.

Many businesses use a rolling forecast approach. For example, if you maintain a 12-month forecast, refresh it at the end of each month by dropping the completed month, adding a new month at the end, and adjusting any figures in between based on what you've learned.

Businesses with seasonal fluctuations or project-based income may benefit from weekly updates during busy periods.

Take control of your cash flow with Xero

Cash flow forecasting gives you visibility into your business finances, helping you spot problems early, plan for growth, and make confident decisions. Whether you're managing tight margins or scaling up, knowing what's coming puts you in control.

Xero makes forecasting easier by tracking your income and expenses automatically and generating forecasts with a few clicks. You can see your projected cash position in real time and connect with apps for longer-term planning. Ready to take control of your cash flow? Get one month free and see how Xero can help your business.

FAQs on cash flow forecasting

Still have questions about cash flow forecasting? Here are answers to some common concerns.

What's the difference between cash flow forecasting and budgeting?

A budget sets spending targets for the future, while a cash flow forecast predicts when money will actually move in and out. You might be on budget but still face a cash shortage if payments don't align with expenses.

How accurate should my cash flow forecast be?

Aim for reasonable accuracy rather than perfection. Reviewing your forecasts against actuals regularly and refining your assumptions over time will help you improve.

Can I create a cash flow forecast if I'm a brand new business?

Yes. Use industry benchmarks, supplier payment terms, and conservative sales estimates to build your first forecast. Update it frequently as you gather real data about your business.

What's the difference between a cash flow forecast and a cash flow statement?

A cash flow statement reports past cash movements that have already happened. A cash flow forecast predicts future cash movements based on expected transactions.

How far into the future should I forecast?

Most small businesses benefit from a 12-month rolling forecast updated monthly. For day-to-day cash management, add a shorter four to eight week forecast with more detail.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.