It’s that time of year again. As summer winds to a close, the days will start getting shorter as the workload ramps up. For those working in payroll, that can only mean one thing: year end is approaching.

There are four key changes in New Zealand payroll calculations for the new financial year:

- Adult minimum wage will increase to $22.70 per hour from 1 April 2023

- The annual ACC earner levy rate is increasing from 1.46 percent to 1.53 percent

- The annual ACC earner levy threshold is increasing to $139,384

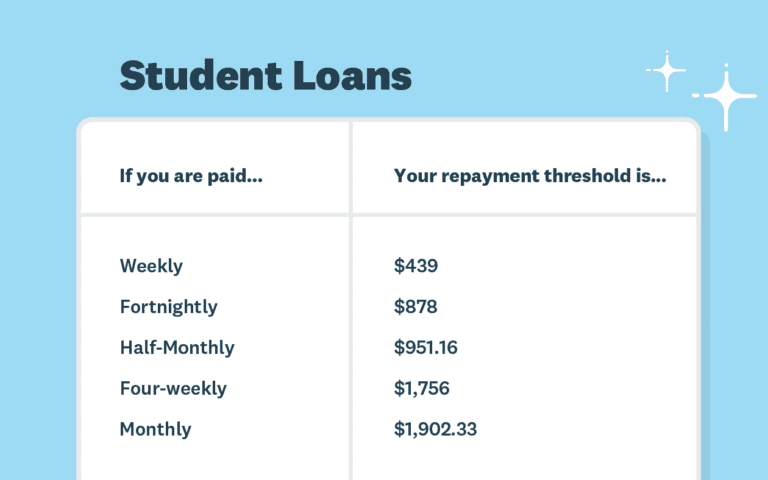

- The student loan threshold is increasing to $439 per week

| The above rates are automatically applied to any pay runs with a payment date on or after 1 April. Your employees may see slight variations in their payslip. |

Step one: Post the last pay run

Make sure all your pay runs for the financial year have been posted. If you’re using payday filing through Xero, you’ll also need to make sure these have been filed. To make sure these pay runs are reported in the 2022 – 23 financial year, the payment date will need to fall on or before 31 March 2023.

Step two: Review and reconcile

Go to payroll settings to review all the information that impacts your payroll reporting. If anything is incorrect, you can update this before processing your first pay run for the new financial year. You can also take this opportunity to check that any final employee payments and changes have been put through.

We know that reconciling your posted pay runs is a regular task for you, but it’s always a great idea to run your eyes down reports like pay history and leave transaction reports to make sure there are no surprises. Here are some tips that may help:

- If multiple expense accounts have been used for earnings and KiwiSaver, make sure the totals are added together and compared against the pay history report.

- Check for any transactions incorrectly reconciled against your expense accounts. You can check this by running the Account Transactions report.

- If your totals don’t look correct, this could be due to some manual journals. Check the amounts by running the Journal report, and then click manual journals.

- If you’re having trouble locating the source of a discrepancy, run your reports for a smaller date range (like monthly) or by each pay period.

Step three: Make any amendments

Any errors made throughout the financial year (such as missed or incorrectly posted pay runs) can be corrected using an unscheduled pay run.

Simply create the pay run for the required period, and enter the adjustment amounts. These adjustments will be filed with Inland Revenue. You can even enter negative values, if needed. If you do this, you’ll need to make sure you log in to myIR to amend the filing, as negative values are not currently accepted by Inland Revenue through payday filing.

Once any amendments are made, check the payment date of the unscheduled pay run falls within the correct financial year, so it’s reported correctly.

Step four: Issue annual earnings certificates

An earnings certificate is a summary of an employee’s earnings, tax and deductions over the tax year. Earnings certificates can be issued to employees at the end of each tax year, or at the end of their employment.

The Accounting > Reports > Earnings Certificate screen allows you to generate and publish earnings certificates, either in bulk or individually. To clarify, employers are not legally obligated to issue earnings certificates to employees; it’s at the discretion of the employer.

Step five: Review and update employee details

- With the increased minimum wage, don’t forget to check and update the salary and wage details for any impacted employees.

- Remember that from 24 July 2021, employees are entitled to 10 days of sick leave as at their next anniversary. So you’ll need to review and update the sick leave entitlements of all employees with an upcoming sick leave anniversary.

- Review current leave entitlements and make any adjustments as necessary – especially if work patterns have changed recently.

- Remember that you need to review and update the ESCT rate for each employee when they start working for you and at the start of each tax year. If your employee’s salary or wages change during the tax year, do not change the ESCT rate during the year. Instead, change it at the start of the next tax year.

You’re done! Sit back and relax

That’s it! There’s nothing else you need to do to finalise payroll year end. Your payroll accounts are now in good shape for the new financial year. Any pay runs with a payment date on or after 1 April 2023 will fall within the next financial year.

In the meantime, check out Xero Central for more information on how to prepare payroll for the new financial year, or register for our payroll financial year end webinar on 2 March 2023. Our friendly support team is also available if you need a hand.

Share this article